Within the first 2 months since the onset of the unexpected pandemic in 2020, attempted unauthorized and fraudulent transactions increased by 35%. If the trend continues frauds due to unauthorized transactions are expected to reach a global high of $40 billion by 2027.

A transaction that was not authorized or permitted by the holder of the concerned account or money is called an unauthorized transaction. It occurs in most transactional and credit card frauds. Governments and financial institutions across the globe are struggling to stop such activities.

How Do Unauthorized Financial Transactions Occur

In the past, most cases of unauthorized transactions occurred as a result of credit card theft. But in more recent years, the majority of unauthorized and fraudulent transactions occur through online portals after the user’s data is stolen through means such as phishing or hacking.

This can happen while the customer or user is providing zis information to a service provider or government portal. The stolen information may lay dormant for weeks or months before the fraudster uses it for an unauthorized transaction.

How Does It Impact The Financial Industry?

Unauthorized transactions are mostly associated with money transfer fraud and credit card fraud. An average of 35% of American consumers fall victim to credit card fraud according to a study from The Ascent.

The issue with this is not just in terms of the financial losses incurred to users and institutions, but also the leak of crucial and private data. The years between 2005 and 2019 saw over 1.6 billion records compromised. By 2020, this resulted in more than $42 billion in losses world wide.This is statistically dangerous for safe transactions and the fraudsters took opportunity during the global pandemic.

It seems that the trend is not decelerating any time soon as is evident from the 161% increase in credit card frauds last year alone. Unless the concerned authorities and consumers take action, the danger lingers. The solution might be more bizarre, yet efficient than we presume.

How Blockchain Technology Proffers The Solution To Unauthorized Financial Transaction

Blockchains are growing lists of records that are linked through cryptography. These records are called blocks and contain a timestamp, transaction data and a cryptographic hash that helps map the data. They are mostly used in cryptocurrencies and their transactions but can be used for other financial interactions as well.

Blockchain is considered secure and tamper-proof while pertaining to digital records. It is a complete and unchanging record of transfers. If blockchain can underpin a payments processing service, it could trace the whole sequence of previous wire transfers.

However, most governments and authorities want a trail of funds to stop money laundering, which is impossible in the blockchain. The whole purpose of blockchain is decentralization and officials demand the source of funds to charge taxes and run governments.

We are experiencing an innovative renaissance in technology. It is only wise to adapt to the changing world. Conclusively, it is not merely blockchain that can help improve financial services, but the numerous options available in technology. But how do we find a good resource provider?

Why Signzy is the Solution For You

Being one of the pioneers in financial and regulatory technologies, Signzy provides you with resources that make processes easier. With an impressive quiver of products and services, we provide you with extremely customizable solutions. These include the numerous APIs and the No-Code AI rule engine we have for you.

Our state of the art Video KYC and Verification solutions are foolproof and secure. If you seek a fortified yet simple process for verification we have multiple APIs for almost all OVD documents including Aadhar, Driving License, Passport, etc. We can help you make your vision of safe, secure and seamless verification processes a reality.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Last year Forbes reported that 2% to 5% of the world’s GDP is laundered every year. This estimates to an amount between $800 billion and $2 trillion. The astounding fact about the report was that only 10% of the laundered money is detected, implying more than 90% of the laundered money is unknown to most regulatory bodies and financial institutions.

Money laundering is a major issue in the world. Governments are striving to find newer methods to tackle it. Most financial institutions and companies are accustomed to traditional methods for preventing money laundering. These include in-person verification or traditional automation.

But with the advent of advanced technologies like AI and Machine Learning, they have to adapt for better results. The latest technology integrated Suspicious Activity Reports(SARs) caused more than 31% of laundered money to be blocked.

Thus the need for technology in preventing money laundering is not a matter of if, but when. But how do we do it? What technological tool can we use? Here comes Application Programming Interfaces(APIs) for the financial industry. This article explores what AML screening solutions APIs are and how they can help in preventing money laundering.

Why Is AML Essential In The Financial Industry?

Anti-Money Laundering includes all measures taken by authorities, institutions and individuals to prevent financial criminals from disguising and hiding illegally obtained money as legitimate income. It is essential as money laundering is a financial crime that affects the economy on a microscale as well as momentous levels. The methods of money laundering are transforming with the development of technology. It is only essential that AML screening solutions up their game too.

In July 1989, many nations came together to form the Financial Action Task Force(FATF). The summit was held in Paris and aimed at analysing laundering risks and preventing them with AML measures and AML screening solutions. But after the 9/11 attacks, in October 2001 the FATF updated their agenda and mission to include modes to stop terrorist funding through money laundering. AML procedures have been made better through the decades since.

The European Union also acknowledged and implemented the first AML directive in 1990. It prevented using the flaws in the financial system for laundering. Now The Union is one of the pioneers in revising and upgrading AML measures to reduce risk and terrorist funding. The International Monetary Fund(IMF) with its 189 member states also takes initiatives for AML with compliance measures for financial institutions. Thus all governments are forced to ensure compliance and all institutions are expected to follow suit.

In 2019 the US State Department published a report stating general AML measures succeeded only 0.2% because of non-compliance and inefficient processes. More than 85% of the 11500 companies evaluated in the US were not AML compliant. 2019 also saw AML non-compliant banks paying more than $6.2 Billion in fines globally.

What Is The AML Process And Why Is Compliance Important?

Government bodies and other regulators provide guidelines and procedures that companies and financial institutions can follow to prevent money laundering.

One of the most important and effective processes is Know Your Customer(KYC). KYC ensures that companies know who their customer is by verifying his financial data with pre-existing credible databases. This way any suspicious activity by the customer can be red-flagged easily.

Customer Due Diligence(CDD) is also a relevant procedure for AML. Companies evaluate the risk involved with each customer and take necessary measures. This is the process of CDD. They categorize customers as low, moderate or high risk. For example, a Politically Exposed Person(PEP) falls under the high-risk umbrella.

Another measure is setting a limit for transactions to be monitored. For example, in the US any transaction of more than $10,000 is reported by the institution to the authorities for monitoring. Each country has such a limit to detect any massive fraud. Thus, monitoring and reviewing customer transactions without compromising privacy is very important to prevent AML. If any suspicious activity is detected, then an activity report is generated and transferred to the Compliance and Risk Department.

It is of incredible significance that financial companies follow all the regulatory compliance guidelines for AML. Even a single discrepancy can result in dangerous repercussions. Money Laundering is no longer just for the money. It can even be used as a wrench in the equilibrium of world peace. Besides this, if companies don’t comply they are charged heavy fines by regulatory bodies. AML fines amounted to $4.27 billion in 2018 which nearly doubled in 2019 to $8 billion. This is a collective effort and even the smallest of the financial institutions need to play their part well by following the compliance guidelines.

How Are APIs Used To Help Prevent Money Laundering?

Software connections between computer programs or even computers are called Application Programming Interfaces(APIs). It offers services to other software once it is integrated into a working system. It can be grossly described as an intermediary software that helps other applications communicate among themselves. They are used in almost all companies with a demand for any form of software technology.

AML screening solution APIs are taking over not just the financial sector, but any industry interested in innovative automation. This is because APIs offer agility and more importantly scalability for companies. Recently, after several government policy amendments, APIs are starting to play crucial roles in AML and KYC compliance. This is because the verification of tens of thousands of customers is not practical with traditional processes.

APIs are used for almost all forms of innovative verification procedures. It ensures that processing is efficient without human error. Since it can be replicated on a large scale, it becomes commercially viable. In addition to this most APIs can be procured at affordable prices. Hence, be it a large bank or a small financial institution, automation is simple and inexpensive. APIs help all businesses Combat Financial Terrorism(CFT) at a modest price.

They are in high demand among elite institutions because they offer swifter and inexpensive methods to ensure services meeting customer demands. Since they are adaptable and customizable, they do get an advantage of future-proofing. In the Financial category alone, more than 2000 types of APIs are used across the globe. This will exponentially grow with advancements in AI, Machine Learning and Blockchain technology.

APIs In AML And Regulatory Compliance

Improved user-friendly APIs are available in the industry now. But it needs to fulfil another crucial criterion for integration into any service or product- Regulatory Compliance. Across the world, there are numerous regulatory guidelines for financial institutions. A good example is the PSD2 changes in Europe. Not only are companies encouraged to accomplish more with AML screening solutions and related technologies, but are fined for any lack of compliance on their part.

Financial Institutions that wait and observe if the new technology trends will be left behind in the race. The most adaptable companies will flourish in the long run. Traditional modes of in-person verification processes and human error packed execution are outdated. APIs can automate almost the entire processes saving companies time and money. On an estimate, more than $500 million is spent by financial institutions for financial crime prevention and compliance requirements.

What Are The Benefits Of Using APIs For AML?

APIs do not merely automate the AML and regulatory processes. They enhance them. There are numerous benefits associated with using APIs for AML and verification processes. They include:

TAT is reduced resulting in quicker processing and better customer journey.

Near zero human error

The extremely customizable nature of APIs makes integration easy.

Inexpensive in the long term.

The human workforce can focus on discrepancies rather than regular workflow, increasing efficiency.

Eliminates all storage spaces as all documentation will be in soft copies.

The better customer onboarding experience

Better user interface

How Can Signzy Help You?

We offer numerous services, products and AML screening solutions APIs that are useful for your ventures. We Make sure that they are state of the art, because we do not compromise quality. Signzy’s quiver of APIs and associated products are incredibly customizable. You can select which specific APIs suit your requirement and then integrate them into the required systems.

With over 240+ microservice APIs alone, the collection is diverse and versatile. All of our products meet regulatory compliance standards without compromise. But we make sure that the user would not be troubled with inefficient customer journeys. Our systems are efficient and seamless rendering the user experience truly satisfying.

With advancing technology financial institutions and companies deem change. If you do not opt for the right changes, the entire entity’s progress would decelerate. That’s why we at Signzy ensure that you get that which suits your needs. We can make your customer’s journeys easy while making your aspirations easier.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Being the 6th biggest manufacturer of motor vehicles, the Indian Vehicular Industry is a behemoth with a $118 billion value estimation. The fact that this is expected to skyrocket to $300 billion by 2025 makes it an unleashed beast.

The current process of customer onboarding and underwriting involves multiple physical parameters with the in-person involvement of the client and the assigned agent. But with novel technologies and cutthroat competition on the rise, it is time insurers decide to upgrade their game. This article focuses on the current market of automobile verification, its challenges and the solution.

The Current Market for Vehicles in India

By 2021 India is expected to become the 3rd largest passenger vehicle market in the world. 2019 saw a 2.7% increase in production in the industry as compared to the previous financial year.

The industry is in a state of growth and it is the right time to take the initiative and utilise it. The current modes of processing can be upgraded with technology. This will help flourish in a cutthroat market like India.

The Primary Players In The Indian Vehicular Industry

There are numerous automobile companies competing in the Indian market. The top ones are:

With revenue of near Rs.300,000 Crore, Tata Motors Ltd. takes the lion’s share of the market. Tata currently has a 6.3% and 45.1% market share in passenger and commercial vehicles sectors, respectively.

Maruti Suzuki India Ltd dominates the passenger vehicles market with over 50% in market share. The Rs.83,281 crore revenue and a market cap of nearly Rs.200,000 crore is an impressive aspect.

Mahindra & Mahindra Ltd also holds a big chunk of the market with revenue heading over Rs53,000 crore and a market cap reaching more than Rs. 70,000 crore.

The two-wheeler giant Hero MotoCorp Ltd comes on top of its specific niche with 36% of the market share. The Rs 32,871 crore revenue and the 57,180 crore market cap is impressive for a primary two-wheeler manufacturer.

Other honourable mentions include Bajaj Auto Ltd, Ashok Leyland Ltd, TVS Motor Company Ltd, etc

What Are The Challenges Of The Industry

As is with most industries, the challenges in the vehicular industry also play a lot in parallel with the adoption of technology. Gone are the old days of physical processing of documentation and verification. With the advancing technology, the terrain is entirely changing.

Insurers must ensure that they can survive the peer competition. Technological services are available for verification and other related processes. But the coding required coupled with the complexity and unavailability of resources from a single portal is frustrating.

Why Is Signzy The Solution?

The solution to technological hurdles is not simply newer technology. It is the right newer technology. Signzy can provide this. With a quiver of products and resources, we can provide you with the state of the art technology while properly understanding your requirements.

Beginning with customer verification using OVDs such as driving license to the verification of the vehicle registration, Signzy’s plethora of APIs will suit you. APIs like DL verification API and Vehicle Registration APIs use government and other databases to cross verify the user’s credibility while maintaining the process seamless.

Since the Signzy portal is extremely customizable you can choose from the arsenal of APIs and other resources. This will help you avoid unnecessary roadblocks. The No-Code AI rule engine that we deploy makes integration and access easy and efficient. Signzy can make your verification processes seamless while maintaining the best security you can obtain.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

With a stunning Compound Annual Growth Rate(CAGR) of 15.6%, the global ID Verification market size is set to grow from USD 7.6 billion (2020) to USD 15.8 billion in 5 years. Along with this, the fraud risk accompanying it will also grow. It is only sensible for financial institutions to take precautionary measures to prevent this.

The first and foremost measure is to ensure the right identity verification services. All successful financial institutions and businesses use a legit and established identity verification service. It confirms that the customer or user-provided information is that of the individual they claim to be by associating it with the identity of the genuine person. The documents used for this can be OVDs like driving license, passport or any national issued document.

With the current trying times, it is important to prevent fraud with the help of such service providers. But the real question is how do you know which one is right for you. In the field of competent marketing, finding a competent service is difficult. This article will simplify that for you by giving you the right parameters to consider while selecting a service provider.

Challenges in ID Verification

Mere identity verification has transformed itself into a digital sphere. This is a result of digitization in all aspects of the financial world. One of the principal reasons for this is the undeniable need for financial institutions to ensure safety from potential fraud and damages. This explains their extensive interest in promoting the safe digitization of their processes.

This coupled with novel databases created by government agencies, institutions and many banks for credit score validation. The initial 6 months of 2019 witnessed 3800 incidents of financial fraud and credit score tampering incidents. This was reported by Risk Based Security. This report, when compared to the previous year’s, illuminates alarming facts. Within a span of 12 months, the number of breaches rocketed 54%.

2019 was also the year with the 3 largest financial data breach, with 3.2 billion confidential records exposed. 84.6% of these breeches originated from the business sector alone. Concerns about safety and security, along with the need for convenience in a competitive playing field, have forced financial institutions and companies to embrace digitization. It is true that the risk of fraud is an imminent and lasting threat. So is the fact that there will be no bulletproof solution.

But we can not expect not to take the necessary precautions and actions. This is why the authentication of customers needs more data and layers of validation. To meet such profound validation criteria while maintaining a good and easy experience for the user is difficult for the institution. Users always have a standard expectation for the products and services they get. To go beyond this is what companies need to make them unique.

While facing these challenges another arises in the form of personal data protection. This has become the penultimate need barring only the actual act of verification. It is an immensely volatile task, but nonetheless a mandatory one.

Considerations to keep in mind before choosing a solution?

The solution to the challenges for a financial institution can be simplified in one word- Digitization. But the pragmatic implementation of this is far more complex without a proper guide. There are distinct steps they need to take before finalizing a verification solution from the numerous ones in the market. These require close scrutiny and articulate decisions. The initiatives to consider while making a choice are given below:

Evaluate the requirements

Maintain the right balance between User Experience, Safety and Security

Acknowledge User behaviour and Channels

Evaluate the Requirements

It is quite apparent that not all cases require the same standards of security validation. But for financial institutions the number of use cases requiring stringent security measures is high. A good example is the provision of online loans and how easy it may seem to the user but how complex it is from the service provider’s part. The process requires information relay and verification through multiple data sources.

The solution is to engage the customer with the right questions. This will give the customer a better experience while obtaining the required data. This implies that the institutions should make proper assessments regarding what information they require. This can eliminate unnecessary steps.

We should assume that more information will be more useful and focus on the right information. Such assumptions sometimes create more friction than what we try to avoid.

Maintain the right balance between User Experience, Safety and Security

Balancing the user experience while obtaining the right information with ease is tricky for even the most advanced procedures available. But it is achievable to a highly optimized degree. Some of the factors to consider while forming different steps in the process are:

Relevance of the data to be obtained

Mode of obtaining the data

Easy accessibility

A good example is setting a threshold for facial verification. Since images will have certain differences, there will always remain a minimal unmatch. Thus a minimum threshold is set. If the threshold is too high, even mostly matching images would be rejected. This will ultimately provide a bad user experience.

The solution to the above conundrum is to have a high functioning AI-driven rule engine while setting a pragmatic threshold limit. This will ensure better customer focus and seamless onboarding journeys.

Acknowledge User behaviour and Channels

An omnichannel presence between the user and the interface is primordial. It will help us understand how the journey impacts the user. We will be able to understand the habits and behaviours of the user. These habits include the use of a phone, tablet or desktop. The journey process must be optimised for each different device.

The verification process should be fit for the channels the company uses. If it is incompatible, then the experience will be troublesome. A good feedback system will help understand the customer’s pain points. Once this is done we can implement a better experience by avoiding any potential hurdles.

What are the parameters of the solution?

Before finalising a solution for digital identity verification, we must always consider certain aspects. The most vital parameters are given below:

The Service Provider’s Technology Quiver

Processing in Real-Time

Ensured Compatibility and Compliance

Efficient Support System

The Service Provider’s Technology Quiver

Multiple forms of solutions are available for identity verification. Each institution requires its own unique set of technological needs. Not every solution provider will be able to meet all the needs of the institution. The development tools to use and methods of integrating 3rd party solutions need consideration.

The service provider’s Software Development Kits(SDKs) or better, Application Programming Interfaces(APIs) should be easy to use and serve a seamless plug and play solution. They should provide products that are understandable to the institution and the user. The identity provider should take care of the underlying technology while maintaining strict regulatory compliance.

Fundamentally, technology should not be a hurdle for the institution as well as the user. It is the responsibility of the provider to make sure of this. Make sure that the services you need are digitally provided.

Processing in Real-Time

Opting for service providers who ensure that most of the processing in real-time is a safer bet in the long run. Not only does this make it harder for any potential fraudsters, but also ensure the right attributes like device location, IP address and avoidance of pre-recorded videos.

The ability to exactly identify the user at the exact moment we require is a boon. The risk of danger is considerably reduced with this feature.

Ensured Compatibility and Compliance

Even though the processing steps vary with each service provider, the regulatory framework demands to have stringent compliance in regards to sensitive and personal information. This is done with proper encryption protocols and interlay with different government and external databases. These can be even international watchlists and credit bureaus.

Verifying and cross-checking the user’s data with the existing databases is essential. This will prevent fraud and validate the credibility of the user. Thus, the relevance of unified data sources is paramount for consideration. A good service provider will keep this a priority.

Updated Support System

The technology involved in digital identity verification systems is evolving. The techniques used by fraudsters to breach these systems are also evolving too. Hence, it is only safe to opt for providers that constantly improve and innovate their services while maintaining newer regulatory standards. They need to keep up with the latest UX and UI trends.

The provider should mandatorily have a live support system for the companies and clients. They should ensure transparent, frequent communication between all parties without any technical difficulties. It will help to investigate the services and products from the provider.

What is the right solution for you?

Now that the parameters to consider while choosing an identity verification service is clear it might seem easier to find an option. But there are numerous identity verification service providers out in the market and only a handful of them are able to maintain exact regulatory compliance and compatibility. Even fewer are able to provide a paragon user experience.

Thus, it might seem arduous to find a service provider who would satisfy all your process demands. You would require an institution with an arsenal of numerous APIs and products.

With a cornucopia of multifaceted APIs, products and service solutions, Signzy has been able to help all our clients in the best ways possible. WIth no-code AI services and smart decision engines, even the back-end operations are smooth with Signzy. With observation and use case histories, even you will conclude the same. If an identity verification service is your need, we can provide the solution through our service.

The logistics industry indulges in the overall process of managing how resources are acquired, stored, and transported to their final destination. Logistics is now used widely in the business sector, particularly by companies in the manufacturing sector, to refer to how resources are handled and moved along the supply chain.

Where Does The Indian Logistics Industry Stand?

The logistics market in India is expected to grow at a CAGR of 10.5% between 2019 and 2025. E-commerce is another major segment that is expected to support the growth of the logistics industry during the forecast period. Increasing investment and trade point towards a healthy outlook for the Indian freight sector.

Who Are The Major Players?

A few of the major players from logistics in India are Allcargo Logistics Ltd.Container Corporation of India Ltd, DHL Express India Pvt, Blue Dart Express Ltd, FedEx, TSCS India Pvt Ltd, Gati Ltd, Transport Corporation of India among others.

What Are The Current Challenges?

Like all other industries, there are several challenges faced by logistics too. A survey was conducted by ByteMaster. After interviewing companies in the transport and storage sector, they concluded that the five main challenges faced by companies in the logistics sector are: traceability, planning, agile procedures, connectivity and deliveries.

Specifically talking about traceability here, it includes tracing of the vehicle details or we can say Vehicle Verification details and with that also tracing the Drivers details for driver verification. A technology partner like Signzy will help you to solve the problem related to the traceability of the vehicle as well as the driver.

How Can Signzy Help?

Signzy has a one-stop solution when it comes to verification. It provides a simple plug and play API solution. With just the vehicle number you can get fitness details, Permit info, PUCC check, Insurance details and much more! The same goes to authenticate the driver’s license.

Signzy can provide a complete user journey and make your workflow simple while it is automated. A generic survey conducted by logistic partners and Signzy showed that automated workflow helped the logistic industry by 26% which earlier with the manual process was 11%.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Signzy’s All-New Quiver Of Premium Products!: With the raging transformations in technology and norms, newer options are set to dominate and revolutionize onboarding. If we don’t keep ourselves ahead of the curve, we might just fall behind in the fast-paced financial industry. Let Signzy help you.

With the numerous modernizations, it is hard for individual enterprises to do this. That’s why it’s always good to seek help from professionals and use proven resources for your business. Signzy brings you the best of both those worlds.

We at Signzy help you keep up with the Joneses by building a global digital trust system to upgrade the current modes in financial technology. While we pursue our endeavour we focus on the ability to uniquely identify and authenticate entities while understanding and knowing more background information about these entities. We create a system of reward and consequences that reinforces trust to help this.

We would love to help you help your business! That’s why we ensure to keep all our products updated to the standard of the future. With our upgraded products, it’s sure that you will find what you seek at Signzy. Some of the major products we offer are included in this blog post.

Every financial enterprise requires an efficient, seamless and safe onboarding solution. This solution must be adaptable to changing technology while maintaining an excellent level of industry-standard safety.

Signzy’s out-of-the-box Generic Onboarding Solution, with an AI-based Rule Engine allows clients to create, update, implement and maintain end-to-end digital onboarding journeys across jurisdictions and business functions. We do this with the maximum assurance of safety and security.

Some of our new features include:

Added security layers to verify that the connections are secure

Extensive search options for back-office processing

A customizable sequence of questions during VCIP calls

The Decision Engine now takes additional final application decisions based on output variables from VCIP increasing straight-through processing rates

Every contract is accompanied by an auto-generated audit certificate for compliance and record-keeping purposes

Apart from the above features we went the extra mile and improved our products for you. The improved aspects are::

Improved user experience for customers including the inclusion of ‘Configurable Text Areas’ to improve user experience and better tracking information on emails being sent to the customer

Additional information to customers on errors – especially in Bank Account Verification

Improved back-office operations experience

Role-based reassignment of application in back-op

Application-level TAT

Additional granularity on the information fetched vs inputs from the user

Making remarks and reasons mandatory for better analysis later

Better security measures

Multi-factor authentication for users

Improved MIS

One column of MIS can possess multiple page IDs

Additional details including TAT captured in MIS for application-level tracking

Some new widgets and APIs were also added to GO. This betters the overall user experience while improving the versatility of the product. They include an SSN Validation API which is now available for US clients and the addition of Generic Delete API. Using the latter, it can be configured that applications belonging to a particular status can be deleted automatically after a set timeframe.

Signzy’s Plethora of APIs to Smoothen Processes!

We have a collection of APIs that will help you in your venture. Though we have many, a few of the latest include:

New Voter ID API

NeSL APIs

E-Stamping

Udyam(MSME) Verification

Vehicle Blocklist and E-Challan Status

…And a complete revamp of our Global KYC APIs

We have also improved upon some of the many APIs already available. Certain of these improvements include the new Name Match API, Aadhar E-Sign API, and an improved Digilocker experience API

Surely, we will not be halting with just these APIs. That’s why we also have more APIs coming your way to improving your venture. These include the E-Nach API, Credit Reports API and the Physical Address verification API.

Signzy’s Video KYC Solution!

Signzy’s All-New Quiver Of Premium Products!: With the new RBI Master Directive, it is inevitable to include the use of Video KYC in any financial onboarding. A good solution will not only help stick to guidelines but dramatically improve customer satisfaction.

Signzy can revolutionize your customer onboarding process and increase the speed to market by 5x. We do it with our enhanced VCIP product- Signzy’s Video KYC Solution!

Latest feature additions include:

Real-time feedback– can address the real-time issues that occur during the call The RE agent gets notified if the end-user is distracted between call

“Uberised” Queues – A better experience for users in the queue, at the same time blocking those ineligible (like location issues)

Detailed MIS reports- are generated and presented. Real-time data regarding RE agent efficiency and queued data are provided

UI Improvements- Multiple improvements have been created to improve the experience

Upcoming releases and Improvements: Signzy’s All-New Quiver Of Premium Products!

In addition to the previously mentioned improvements, we are working on a lot more for you. These new features will come to your doorstep in the not too distant future. Below are a few of them to give you an idea:

Skills-based auto-assigning agents to the users

MIS reports with detailed analysis of all the video calls, agents’ productivity, call improvement etc.

Conditional rendering of options in real-time feedback for agents

Rescheduling the call to be made configurable

Configurable option to automatically set the offline/online status of RE agent

Revamping the rescheduling system to a better version.

Conclusion

In order to keep up with the newer norms and trends, institutions and companies are forced to adapt to new technology. As it becomes mandatory to accept the change, why not use it to your advantage? Why not understand what is needed and make it far better?

This is exactly what Signzy will do for you. With the numerous products, resources and services we provide, we can certainly make your business smoother and easier than ever before. The right direction with the right people will lead us all further to our goals.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Isn’t this the first question that comes to one’s mind when meeting a person for the first time? It is a natural question. In people’s conversations, a response is enough to close this question. But, it is different when dealing with institutions like Banks, Countries (immigration officers), and governments. Verifiable documentary evidence has to support the response. This is when an Identity Verification Service comes into play.

It doesn’t matter who you are. Documents must validate identity when dealing with institutions. A couple of years ago, a video went viral on the internet. It featured the tennis great Roger Federer. An usher at the Wimbledon center court did not allow Federer to pass without an ID document. For the record, Federer has won Wimbledon a record 8 times.

Businesses use identity verification services to ensure customers’ identity is true and accurate.

The identity verification service validates identity in the following ways

Using Government documents such as license, social security card, or passport.

Verify information from many sources – credit bureau or government databases.

Thus, identity verification service ensures successful KYC and Anti-Money Laundering (AML) compliance. It also reduces risks by fighting identity theft.

Your business may not have an identity verification service in place. It may already have one but is evaluating other options. Here are pointers to build a strong, successful, fintech, and sustainable identity verification process.

Compliance for an identity verification service

Law of the land still reigns supreme. Statutory and regulatory compliance is mandatory and no exceptions are advised for any identity verification service. On one end, there are KYC requirements that mandate access to identity, financial and personal information. On the other, there are privacy laws that regulate access to user-owned data. A paradox. It is this contradiction that identity verification service providers have to navigate.

KYC

In 2002, all financial institutions made KYC mandatory in the US. This was due to the USA Patriot Act of 2001, which came into being after the 9/11 tragedy. All KYC processes have to adhere to a customer identification program, called the CIP. The CIP also forms part of the institution’s anti-money laundering (AML) policy. Banks and Fintechs leverage KYC to assess customer profile and consequent risk.

Privacy Laws

On 25 May 2018, the European Union (EU) put a privacy law into effect – General Data Protection Regulation (GDPR). GDPR brought to the forefront the entire debate on data privacy. ‘User consent’ is the cornerstone of GDPR giving tremendous control to the user. The user now has the power to manage data – active and passive – that the user shares with other parties. The US too has many privacy laws, but none at a central federal level, unlike the EU’s GDPR. The Californian Consumer Privacy Act (CCPA) is often the most talked about and the most recent.

Be aware of legal requirements before zeroing in on an identity verification service. Adhere to all laws including KYC, Anti-Money Laundering (AML) regulations, and privacy. Violation of laws could invite major penalties or financial jeopardy.

Fraud Protection

The leading identity verification company Idology published the eighth “Annual Fraud Report 2021.” It says leaders call identity verification, the number one challenge in addressing fraud. It is not surprising. Covid-19 accelerated digital transformation initiatives across organizations. Identity verification was one of the top use cases. This at a time when incidents of fraud – financial, data breaches, identity thefts, and mobile fraud plays – are at historical highs.

Technology

Without technology, no identity verification service would be possible. The options are discussed below.

Optical Character Reader (OCR)

The world is still far away from complete digitalization. Most documents including those related to identity are still in paper form. OCR transmits the data from paper to electronic portals. OCR scans, recognizes, reads, and extracts written information from an identity document. It then verifies if the identity card submitted by the customer is legitimate or not. This allows customers to verify their identity through smartphones. OCR collects data from documents and encrypts it to follow regulations and reduce fraud.

Biometrics

Your smartphone asks for your fingerprint or your Face ID to unlock. Biological markers are impossible to replicate. These markers are best placed to customers into a password.

Biometrics goes beyond face id recognition. It could extend to DNA matching, iris scan, fingerprinting, voice, and even typing. Biometric identification captures and corresponds to people’s unique physical features/behaviors. Thus, it lends strong confidence to a business’s approach to identity verification.

Blockchain

Following the crypto-mania? The Bitcoin frenzy has overshadowed the technology that powers crypto – Blockchain. Blockchain is powering a broad range of applications from trade to music and even voting. Yes, voting in elections. Identity management is using blockchain too.

The beauty and strength of the blockchain are that it restores the right to privacy to the user. It is the user who decides what personal identity information to share. Thus, fintech balance the challenge of ensuring compliance while adhering to privacy laws.

Blockchain is a digital ledger of decentralized data. It lends itself well to solve the use case of identity verification. Consumers assign a digital identity or watermark for all transactions. They then decide which information to share. This makes the process speedy, convenient, and risk-free for both parties. Thus, leveraging blockchain technology can ensure that digital compliance is convenient yet secure. Digital identity verification solutions including Signzy are also utilizing blockchain to audit transactions.

Artificial intelligence (AI)

AI impacts identity verification in the following ways,

Replace the human in performing all mundane tasks e.g. physical verification of paper identity documents.

Quick real-time verification of captured information with a trusted database either public or private.

Fraud detection and prevention.

Artificial Intelligence (AI) fastens the identity verification process compared to humans. It also resolves the biometric issues related to aging, makeup, and facial hair. AI-driven platforms leverage artificial intelligence algorithms. They verify a selfie and a photo ID for a swift and accurate identity verification process. AI accepts many identity card formats and uses the selfie for more authentication. AI conducts real-time authentication with geolocation, IP address, and AML background check.

The technology stack supporting identity verification could start with one of the above. The stack could also be a combination. The decision would depend on the requirements and the business’ capability maturity. The choice of the technology stack should address compliance, fraud, and user experience.

Awesome User Experience (UX)

Identity verification is fraught with friction. In most cases, it is a frustrating experience for the users. Most users seem to have developed ‘acceptance’ to a poor user experience. Even the smallest convenience offered comes out as a great user experience. Balance awesome UX with the need for compliance and also preventing financial frauds.

Factors to consider

The approach to delivering a great UX could be guided by the following factors.

Avoid human intervention as much as possible

Ever imagined what would happen if the number of customers increased by 10 times? Wouldn’t it be tedious for your staff to keep up with the onboarding process? Thus, it would lead to bottlenecks causing the process to slow down. Higher the number of customers, slower the onboarding process. It’s an issue that can be exacerbated. Hiring more employees could solve this problem but wouldn’t be beneficial. Deploying automation will prevent this problem. It will avoid time-consuming processes, human errors, monotonous and repetitive tasks, improving productivity.

Need for speed and seamless experience

Customers hate waiting. The more you make them wait, the higher are the chances of you losing them. Sign-up abandonment is a reality, even if related to ‘mandatory’ services like banking. Unfamiliarity with the processes can be uncomfortable and frustrating for the customers. This causes poor user experience, resulting in abandonment and even churn.

Set user expectations

Identity verification is never a one-step process. It has to involve many steps. Setting user expectations at the outset can help manage user expectations better. Resetting user expectations at every step will help build a relationship. Thus, leading to eventual success.

Quick Wins

The single most important element in improving UX is simplicity. Achieve UX Simplicity by doing some of the following.

Autofill or automate the capture

One can’t imagine the joy one experiences on seeing a 15 field form partially auto-filled. A helpful dopamine shot. The availability of public and private databases of information can improve UX and cut errors of omission and commission.

Ask easy to remember information

Instead of asking the entire 9 number social security number (SSN) asking for the last 4 digits could catalyze action. Similarly, asking for information progressively (i.e. step by step) instead of all at once could reduce friction.

Fallback

Not every user who fails verification is a fraudster. Legitimate users may also be unable to verify ID because of genuine reasons (patchy internet, poor quality camera). So as not to impair UX, the system should provide for a fail-safe fallback including a manual process as the last option.

It is all coming together

Digitization will continue to grow. Institutions will juggle many factors in implementing identity verification solutions. Compliance will, without doubt, be the overriding factor in setting direction. E.g. The current COVID-19 pandemic is exerting another layer of verification for people’s movement. The continued growth in mobile users is making awesome user experience hygiene. UX should be as simple as ordering food on mobile, if not simpler. It is up to technology to do the tough balancing act between compliance and UX. It will be interesting to witness the future of digital identity verification. It will include compliance, mobile identities, cross-border imperatives, and artificial intelligence. Get ready for a machine soon asking you, “Who are you?”

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The Reserve Bank has always tried to remain adaptable in changing times. Its directive to utilize a video-based customer identification process(V-CIP) for know your customer (KYC) procedures is the latest evidence for this. The announcement came as an amendment in its master direction on the 10th of May 2021.

V-CIP utilizes facial recognition technology to identify the customer. It can also include an authorised official from the regulated entity (usually an RM) performing the live customer due diligence with informed consent for verification. This is far more convenient, secure, and seamless since the whole process is an audio-visual interaction between the RM and the customer.

What Is The RBI’s Directive?

The Reserve Bank stipulates regulated entities(RE) to use V-CIP in Customer Due Diligence(CDD) for:

New individual customer onboarding.

Proprietors(Proprietorship Firms)

Beneficial Owners(BOs) and authorised signatories among legal entity customers.

The directive is also for other RBI regulated entities including banks, payment system operators and NBFCs. Updation of KYC for existing customers and customers who had opened accounts through non-face-to-face modes( Using Aadhar OTP based e-KYC verification) is also to be done with V-CIP.

The RBI provides guidelines for a minimum standard for all REs to maintain baseline cybersecurity for banks and financial institutions. These include them:

House all technology infrastructure in the RE’s premises.

Use secured network domains for V-CIP connection origins.

Ensure all outsourcing of technology associated with the process to be compliant with respective RBI guidelines.

Maintain end-to-end encryption of information between V-CIP hosting point and customer’s device.

Obtain auditable and alteration proof customer consent.

Create a transparent workflow and SOP(standard operating procedure) for all V-CIP related processing.

REs should appoint specially trained officials for operating the V-CIP process. These officials would record audio-video and obtain photographs(mostly real-time) of customers whose identification is to be verified.

These officials can obtain the customer identification information with an Offline or OTP based Aadhaar e-KYC verification. They can also retrieve the required information from CKYCR or equivalent OVD e-document repository through DigiLocker.

How Will It Impact The Sector?

Many financial institutions have already taken up V-CIP as an additional armour of protection against fraudsters and scammers. The RBI’s amendment of the master direction will further encourage more institutions and REs to adopt V-CIP. The usually hesitant players will adopt this mode of technology for their benefit. Even the traditionally slow to adapt government sector banks and NBFCs will also follow suit.

The change would not only affect the REs and institutions, but also the customers in a rather positive fashion. With the pandemic looming over the country, every individual desire to be safe and avoid all in-person interactions. With this directive, the REs and financial institutions are compelled to help solve this issue. With remote V-CIP methods, all customers will be at zero health risk.

Additionally, no customer prefers the extra time commuting and the plethora of documentation formalities that may follow in legacy systems of CDD. V-CIP makes the journey easier, preferable and convenient for the customer, all while saving the REs and their employees time and resources.

But it is important to be aware of how REs avail V-CIP services from Regtech firms. When it comes to such crucial aspects it is always safe to bet on reliable and supportive companies for assistance.

Why Signzy?

Signzy is a ‘no-code AI platform’ for financial services. No matter how complex a workflow or an operation, Signzy can completely automate the back-office operations and decision-making processes into a real-time API. Signzy’s pantheon of V-CIP related products is efficient and reliable to another class.

Some of the features Signzy’s V-CIP and Video KYC products have are:

Real-time OVD verification

Matching face on ID with face in the video (with % confidence score)

Unlimited video storage and instant retrieval

Geo-location capture and IP check

End-to-end encryption for video, channel, and communication

Video forensics for pre-recorded risk and spoof detection

Digital forgery check on the displayed ID proof

Customer identity verification through offline Aadhaar XML

Seamless and interactive UI for live video interaction

Timestamp and audit trail for every application and video interaction

Signzy’s V-CIP services and products are 100% in compliance with all the RBI regulatory guidelines and directives. This is essential as all REs are supervised for the right compliance practices and Signzy offers to negate all possible complications. Signzy’s solutions are easy to use with immediate responses which make it fast and efficient.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Know Your Customer, is essential in the online gaming realm to ensure the integrity, safety, and compliance of the platform. As the digital gaming industry expands, it’s imperative to verify the identity of players to prevent fraudulent activities, underage participation, and potential misuse for money laundering.

The global online gambling industry was worth more than $45 billion in 2017 and is predicted to rise to $94.4 billion by 2024. With such a stark rise in use and increasingly large sums of money moving through these entities, online gambling and gaming institutions are facing the same scrutiny to which other banks and other financial entities are subject. Prime targets for identity fraud, money laundering, and international financial crime, regulatory compliance is intensifying to ensure that online casinos and gambling institutions are taking serious measures to prevent such illicit activity.

However, as the demand for online gambling services increases, so does the stringency of regulatory compliance. Not only does this mean hiring a large compliance team to deal with the backlog, but online casinos are also now subject to higher costs and wait times for identity verification procedures. In this sense, manual KYC processing for casinos is a little outdated, offering a clunky solution that wastes time, squanders budgets, and is littered with errors.

In the USA, online gambling establishments that have gross revenue of over $1 million are classed as non-bank financial institutions (NBFI). This means they must adhere to similar regulations as banks to help prevent fraud, financial crimes, and money laundering.

The Financial Crimes Enforcement Network (FinCEN) is responsible for monitoring the compliance of AML regulations under the Bank Secrecy Act (BSA). The BSE requires that financial institutions must help the government identify and prevent money laundering by identifying, flagging, and reporting certain suspicious activity and transactions. FinCEN has assigned this responsibility to the Internal Revenue Service (IRS) to ensure compliance measures are being met.

For relevant online casinos, AML measures include filing suspicious activity reports (SARs) for unusual transactions of over $5000, as well as reporting currency transactions of over $10,000. There are also extremely tight requirements for recordkeeping and receipt storage, as well as credit extensions over $10,000.

While all of these AML measures are a must, US online casinos are first required to accurately identify and verify customers using KYC processes. Failure to do so results in unbelievable fines.

In fact, the American Gaming Association (AMA) recently updated its policies. According to these new regulations, US users can not open an account without providing basic PII details: full legal name, address, and social security number. More importantly, however, no real money transactions can be undertaken without submitting an official government ID and proof of a permanent address.

The poignant point here is that AMA’s rules apply to the patron, not the casino as such. In this sense, a US citizen using an online casino in a different jurisdiction must still provide this information. If online gambling platforms don’t have measures in place for this, they are in danger of non-compliance.

Call For KYC In The Gaming Industry – How It Can Help?

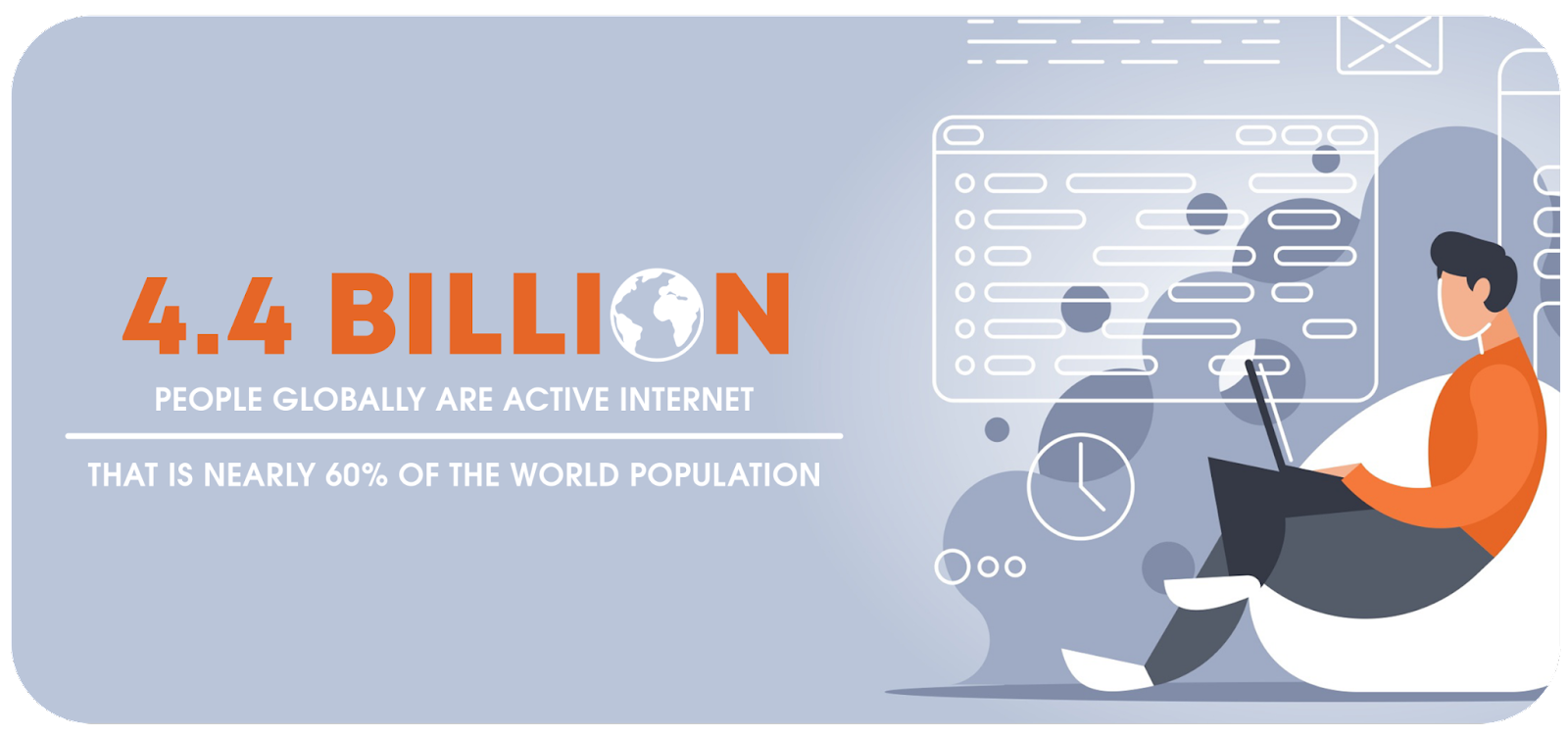

Almost 4.4 billion people globally are active internet users as of April 2019. This means that nearly 60% of the human population has the means to connect and interact with the online world around them. It’s no surprise that these combined factors have fueled the market for online gambling and gaming. In an already heavily regulated marketplace, this rapid growth is bringing Know Your Customer (KYC) and Anti-Money Laundering (AML) to the forefront of regulators’ agendas around the world.

With a wide range of options for users to gamble online, it makes sense that the companies that will come out on top are going to strike a balance between compliance and user experience. The question is, how can companies maintain compliance without sacrificing an incredible gaming experience for their users?

Why do online gambling and gaming companies need to be responsible for KYC?

Companies in the online gambling and gaming industries are legally obligated to verify user identity, age, location, and source of funds among other categories to protect their users and platform from bad actors and fraud.

One of the major reasons for this is the need to avoid money laundering and terrorist funding. If proper KYC is not performed on contestants and participants, the platform can be used to launder money and use it for assimilating funds for dangerous organizations. Many laws are created to prevent such practices and most gaming organizers and companies must abide to it.

Just as reputable companies prioritize trust when it comes to providing users with fair play and a secure environment, users must be able to trust that information being collected from them is being handled appropriately and safeguarded.

Companies looking to stay both in compliance and competitive are seeking advanced onboarding & identity verification solutions to…

Protect the company and users from bad actors and fraud

Continuously comply with the latest global regulations

Deliver a seamless, trustworthy, and user-friendly experience

KYC in The Gaming Industry – Mistakes That Could Be Avoided

Casinos deal in financial transactions, often on a very large scale. Online gambling platforms and casinos can turn over millions of dollars a day, making them a prime target for money laundering and financial crimes. Not only that, the lack of face-to-face interaction on internet gambling platforms makes it easier for fraudulent users to play on these sites without detection.

KYC and identity verification processes are designed to help reduce the risks of illicit activity by identifying customers and verifying that this identity is correct. In doing this, suspicious characters and potentially high-risk users can be flagged and monitored, or banned.

As in every industry, a risk-based approach is very important and necessary in the gaming industry. For an AML control program to achieve its purpose, it is very important to identify risks and take precautions against risks. As part of the risk-based approach, game operators must implement risk assessment by implementing AML controls to new customers throughout the customer engagement process. Know Your Customer and Customer Due Diligence procedures describe the controls that must be implemented during the customer onboarding process.

Currently, it’s predicted that 2-5% of the US’s GDP is laundered money, equating to between $800 billion and $2 trillion. Unfathomable sums of this nature have the power to shake the bedrock of the US economy.

While money laundering may seem to be a primary concern for banks and financial entities, studies show that casinos are ripe for money laundering. In 2014, Finnish gambling operators submitted over 9000 money laundering reports.

Studies are showing that criminal groups, known as dot.cons work together to ‘wash’ funds by deliberately losing games and claiming ‘clean’ prize money. A great example of this was The Corozzo Network, operating from 2005 to 2008. The network of 26 members ran illegal gambling and loan-sharking services through four online gambling sites, laundering more than $10 million.

More recently, CG Technology (trading as Cantor Gaming) was fined $22.5 million by various regulatory bodies in 2016 for poor AML provisions. The gambling company’s lack of AML procedures enabled 26 individuals, known as the ‘Jersey Boys’, to launder large sums of money through the platform with bad bets.

Further still, as technology advances, the schemes become more complex. Thanks to the introduction of virtual credit cards, prepaid mobile credit, and alternative payment gateways like PayPal, micro-laundering is now easier than ever and far less detectable.

By introducing strict KYC checks, casinos mitigate the risk of becoming vehicles for money laundering as high-risk individuals are flagged from the outset.

How Digital KYC Can Help The Online Gaming Industry

As we can see from above, KYC and AML (Anti Money Laundering) solutions can save business owners a lot of hassle. Digital KYC systems would have carried out comprehensive background checks identifying possible threats and allowing the owner to take action accordingly. The online gaming industry is a hotspot for money laundering although certain policies are governing the industry the chance is still there that it could be used for terrorist funding.

Signzy is an AI-powered RPA platform that provides digital onboarding solutions with our no-code AI model builder and our Fintech API Marketplace of over 200+ APIs. Our unique solution provides:

Secure System: A customer’s account information is secure because the entire process is online. Identity theft, fraud, loan scams, money laundering, the flow of black money, etc. are all minimized with RealKYC.

Efficient Communication: Effective information can be relayed in an efficient and timely manner. There is no need for constant back and forth. Most details are published automatically unlike manual KYC.

‘Free of Cost’ Process: RealKYC verification doesn’t charge any extra amount to the customer. A company or institution may need to pay automation costs of installing verification systems for the long run but the end-user gets a seamless, almost instant onboarding without hassle.

Faster processing: The RealKYC service is completely automated online. This means that KYC data can be transferred in real-time without the need for any manual intervention. The paper-based KYC process can take days up to weeks to get verified, but the eKYC process takes just a few minutes to verify and issue.

At Signzy, we have also introduced a new form of KYC verification called VideoKYC. This is a faster and more efficient form of KYC collection and verification. It conducts liveliness checks against the user as well as verifies the identification document against forgeries. The VideoKYC product has gained a lot of recognition and won several awards in recent months.

Advantages of using VideoKYC

Higher Application Accuracy

Plug and Play solution, swift Go-To-Market

Comprehensive Training Program

Competitive Advantage through customer delight

100% compliant with the latest RBI Mandate

Exponentially increase Scale of Operations

Reduced back office overheads (up to 70%)

Reduction in customer Drop-offs (up to 50%)

Platform Agnostic, support multiple communication channels

Conclusion

The online gaming industry is evolving rapidly around the world and expanding with each passing day. Gaming sites have improved tremendously in terms of user experience and now, they can make it more secure by enhancing the membership security protocols. Providing different gaming sites the ease of accurate digital ID verification will increase their revenue manifold. The introduction of digital KYC services has already been a huge success in financial and other sectors. Hopefully, its adoption in the near future might lead to more secure online gaming services in the US.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The base for data privacy and protection is crucial for an upcoming data-driven economy like India. India hosts almost 450 million Internet users and a consistent growth rate of 7–8%, as per Forbes. The transition to a digital economy is radically underway. However, this implies that the processing of personal data is already on the verge of becoming universal.

The population of mobile phone users in India has already crossed the 750 million mark. This number is expected to reach 490 million by 2022. Therefore, personal data and information become available in the public domain. Sources estimate that India has about 390 million millennials and about 440 million generation Z that follows millennials.

The Gen Z generation processes data faster. The most common use of this data is for mobile applications like Snapchat, Vine, and so on, apart from the usual popular social media apps. This leads to the creation of huge amounts of personal data for an individual — be it personal, behavioral, attitudinal, and financial. Which can essentially be used for both illegal and nefarious purposes, like what happened with Cambridge Analytica; Hence, data privacy will be of paramount importance in the coming years for governments across the world specifically to protect their citizens.

The IT Act 2000 — The First Ancestor Of Data Privacy

Under section 43A of the (Indian) Information Technology Act, 2000, a body corporate who is possessing, dealing, or handling any sensitive personal data or information, and is negligent in implementing and maintaining reasonable security practices resulting in wrongful loss or wrongful gain to any person, then such body corporate may be held liable to pay damages to the person so affected.

The Government of India has ratified the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011. The Rules provide guidance against protection of “Sensitive personal data or information of a person”. This consists of such personal information which has information relating: –

Passwords

Financial information — Bank account or credit/debit card or other payment instrument information;

Physical, physiological, and psychological health conditions;

Sexual orientation

Medical records and history;

Biometric data.

Section 72 of the IT Act highlights the penalty for breach of confidentiality privacy. The Section provides that any person who, in pursuance of any of the powers conferred under the IT Act Rules or Regulations made thereunder, has secured access to any electronic record, book, register, correspondence, information, document, or other material without the consent of the person concerned, discloses such material to any other person, shall be punishable with imprisonment for a term which may extend to two years, or with fine which may extend to Rs 1,00,000, (approx. US$ 3,000) or with both.

While the IT Act 2000 was not officially cleared for regulating data privacy in India. It can be considered as the stepping stone which laid the foundation for future legislature.

The Supreme Court Ruling of 2016- Amendment Of Data Privacy In Aadhaar Act

In 2016, India amended its biometric identification system, known as Aadhaar. This enabled both the government and private entities to collect an individual’s ID number for any purpose. Human rights advocates had decried this as a violation of privacy. There was a lot of concern and growing uncertainty surrounding this authorization. However, businesses in India continued to require ID numbers for certain services. It was also used for the ID numbers for consumer profiling and targeted advertisements.

The Supreme Court of India amended the 2016 Act which enabled private businesses to ask for customer ID numbers for any purpose. The Supreme Court was required to ascertain the validity of the provisions of the Aadhaar Act. The objective was to verify if the act was contrary to the right to privacy. This was later established as a fundamental right by the Supreme Court in 2017.

Key Findings in the Judgement

The judgment was unanimous with all nine judges concurring with the final order. However, six judges — Justice Chandrachud, Justice Nariman, Justice Chimaleshwar, Justice Kaul, Justice Sapre, and Justice Bobde, wrote separate opinions covering a wide range of issues.

The key points of the judgment are summarized below:

(a) Privacy — A Fundamental Right

The Supreme Court confirmed that the privacy rights of an individual are a fundamental right. It does not need to be separately articulated. It can be considered as a derivative of articles 14, 19, and 21 as mentioned in the Constitution of India. It is a right that subsists as a fundamental consequence of the right to life and liberty. It protects a person from the scrutiny of the State in their home, of their whereabouts, etc.

The same applies to more personal choices like reproductive choices, food habits, etc.

(b) Necessary But Not Absolute Right

The Supreme Court also highlighted that the fundamental right to privacy is not absolute. It will always be subject to considerable restrictions. The State can declare restrictions on the right to privacy to protect justifiable State interests. This can only be done by following the three-pronged method summarized below:

Establishment of a law that rationalizes an encroachment on privacy

A legitimate State aim or requirement which ensures that the nature of the composition of this law falls is reasonably valid. It should also operate to guard against arbitrary State action.

The measures taken by the State are in tune with the objectives sought to be fulfilled by the law.

The Personal Data Protection Bill — India’s First Step To Legalize Data Privacy

Backdrop of The PDP Bill — How it came about

The Supreme Court observed during its judgment that privacy of personal data and facts is an essential aspect of the right to privacy.

Based on this, the Ministry of Electronics and Information Technology (MeitY) formed a 10-member committee led by retired Supreme Court judge B.N. Srikrishna. This committee was hence named the Srikrishna Committee. On 27 July 2018, the committee submitted an extensive draft which is now known as the Personal Data Protection Bill. India is now set to have a comprehensive personal data protection law. On 11.12.2019, MEITY introduced the Personal Data Protection Bill (PDP Bill) in Lok Sabha as Bill №373 of 2019.

The Birth Of PDP — India’s Data Privacy Bill

The PDP Bill seeks to provide for the protection of the personal data of individuals. It also intends to create a framework for processing such personal data. To do so, the bill proposes the establishment of a Data Protection Authority.

Key Takeaways of The PDP Bill

The following are the salient features of the Bill:

The PDP Bill is meant to improve data handling and data privacy in a way that is similar to the European Union’s GDPR.