Acquirers are always struggling with the cumbersome merchant onboarding process. The need is of an enhanced digital merchant onboarding experience. A platform that is agile. A platform that supports a 100% automated onboarding.

One that incorporates checks for fraud and Anti Money Laundering (AML), digital Know-Your-Customer (KYC), and risk decisioning. Digitizing the process is the solution for faster onboarding and better compliance.

3 Key Problems with the Traditional Merchant Onboarding Process

The traditional merchant onboarding process is frustrating and siloed. This means that each linear step is isolated in its functioning. An inordinate delay of about a week could come up to complete the application process. There is no status monitoring process which could track applications end-to-end. In the short term this could choke operational excellence. In the long run threaten business growth.

Existing data entry systems used for traditional onboarding are manually-driven and painfully slow. The process is susceptible to human error and can result in squandering of days of time. It could cause rampant inaccuracies in the entered data. The situation is extremely precarious because data inconsistency could prove to be detrimental to user privacy and the reputation of the business. Trust cannot be built in a system prone to error.

Merchant onboarding journeys are tedious, long and inconvenient. They stretch across numerous drawn out touchpoints and channels. This leads to excessive service delays lasting up to days or weeks, and poor customer experience. In case of an error the to and fro communication causes further delays.

These key problems thwart any chance of a seamless process. They peak their heads in the following 3 friction points, which slow down and complicate the merchant onboarding journey. This section explains what they are and how the digital onboarding process can solve these issues:

Friction point 1: Manual Form Filling

Data from physical paper applications has to be manually put into the computer database. This requires considerable effort from many physical operators. Significantly reduces errors by eliminating as much manual data handling as possible. This is a common source of error and denied applications. An AI based OCR (optical character recognition) performs extraction at the front-end. It is optimal to reduce time and error. With this, it is now possible to fetch customer information by extracting it from their IDs. The field filling process is also automated. This reduces the mistakes which were made by individuals filling the application. The cumbersome need for manual form filling is eradicated.

Friction point 2: Time-consuming Document Verification

Significant diligence checks and third-party verification is needed to ensure merchants aren’t involved in fraud. The solution must validate the authenticity of documents as part of the onboarding process. When this is done manually it takes huge amounts of time. It is also prone to human error. If additional details are required like court history, there emerges another layer of research. With digitization it is just a matter of ticking the box for another method of verification. Details are then pulled automatically from the Ministry of Corporate Affairs (MCA) database and tallied.

Friction point 3: Risk Assessment/ Underwriting

Information collected in the application paired with a rules-based engine is what decides if an account is approved or declined. The rules-based verification engine determines whether or not a merchant is a pass/fail. According to the required verification needs, data can be retrieved on the merchant very fast. An interactive scorecard or report needs to be made. Organizations generally have access to required data. The question is how do they automate the process and stitch it all together. Risk assessment done manually is arbitrary. But, an automated process has set parameters.

Major Advantages of this Solution

Smoothening over these 3 friction areas results in a host of benefits. They can be boiled down to the following three advantages:

Taking down Time

With automated onboarding abandonment is largely avoided due to the simple process. It cuts through red tape and desk delays. Even in the case of insufficient information, the merchant can be contacted and details clarified without leaving the house. Apart from that, merchant onboarding solutions like Signzy empower a business to create easy real-time processes without sacrificing the risk strategy. A customizable fully automated onboarding process that meets all compliance and KYC regulations can be created with Signzy tools. Whether it’s a straight through process or more complex processes to verify high-risk merchants decisions can be made in real-time. For a merchant, the need to spend hours in filling applications is eradicated. For banks, the verification of documents is expedited with some automation.

Curbing Cost

Digitization with an onboarding solution successfully streamlines the merchant onboarding process to the point where the merchant doesn’t have to even speak to anyone to set up. With manual data entry not required and the time taken to process the applications at the backops drastically reduced, the operational expenses of onboarding come down.

Lighter Labour

A major pain point for the industry is manual work like data entry. The work is often done multiple times. Manual work slows down the process. It can also introduce points of failure in the system. It adds a significant cost to the process. This should not be translated as eliminating people from the process. But, people should concentrate human effort on identifying fraud. Data entry is easily automated. Automation also enables smoother integration between the steps. If data is digital from the start, then the entire process has the potential for automation, especially in the case of smaller merchants. New risk assessment automation, as well as integration and optimization tools, are on the market, so dramatic improvements are already possible.

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Digital KYC verification has made CASA banking really simple. Let’s understand how….

A current account savings account (CASA) is a combination of the features of savings and current accounts. It enables customers to keep their money in the bank. It provides very low or no interest on the current account. For savings accounts, banks provide an above-average rate of interest.. A CASA functions like a normal bank account where funds may be withdrawn at any time.

Most banks provide CASAs to their clients for free. In some cases, a small fee may be levied, based on certain minimum or average balance requirements. A CASA tends to be a cost-effective method for a bank to raise money. This is a more suited alternative to issuing term deposits like fixed deposits (FD). FDs offer higher interest rates to customers.

Financial institutions prefer the use of a CASA as it generates more profits. The interest paid on the CASA deposit is less than on a term deposit, the bank’s net interest income (NII) is higher. Thus, CASAs can be an effective source of funding for banks.

Banks and regulators have focused on eradicating terrorist funding and money laundering. The objective is to prevent financial terrorism related activities. It’s impossible to transfer funds around the world and within a country without using a financial institution. As such, banks have increased their efforts to prevent, detect and report suspicious transactions. These include financial transactions that are connected with money laundering and terrorist financing. Digital banking KYC verification is a critical component to anti-money laundering efforts.

As per RBI regulations on KYC, the objective of KYC/AML-CFT guidelines is to protect banks or Financial Institutions (FIs). This prevents them from being used by for money laundering or terrorist financing activities. KYC procedures also enable banks and FIs to know and understand their clients. This helps in their financial dealings better, and so manage their risks prudently.

KYC is a fundamental part of the banking process. KYC regulations are non-negotiable and non-optional. This applies to retail banking as well as corporate banking,

In simple terms, KYC in CASA involves four essential steps:

The customer identity: This can be Individual, Partnership, Sole Proprietorship Firm, Company, or LLP

The business’ address: The registered address where business activities are being carried out. For instance offices, factories, depots, or warehouses

Statutory registration: The business is compliant with various statutory registrations under RoC, Income Tax, GST, etc

The legality of the business: Whether the business is legal as per Indian laws.

The KYC process in banks is elaborate and time-consuming. This is because it involves a lot of documentation, compliance checks, and background verification. The process can take 2–3 weeks to be completed and also imposes an enormous cost to banks and FIs.

Although it is a legal mandate for banks and FIs, conventional KYC methods provide a miserable experience for customers. Banks and FIs have switched to technology to enhance the KYC processes. Ideally, customer interaction and contact is barely needed for KYC. This is due to the fact that most data are available on the public domain. Asking the customer to submit the same data inevitably delays the process.

USA

In 2016, the U.S. government passed a rule which mandates banks to verify the identities of beneficial owners of legal entity clients. These include corporations, LLCs, partnerships, unincorporated non-profits and statutory trusts. Beneficial owner information is necessary for an individual. This is applicable for individuals with an ownership stake of 25 percent or more equity interest.

If you’re a beneficial owner of a legal entity, the following personal information must be furnished that includes:

• Full legal name

• Date of birth

• Current residential address

• Social security number (SSN) or other government issued identification number for US citizens

Banks and other financial institutions must procure this information. This is because it’s a regulatory compulsion. It attempts to prevent, detect and report money laundering and terrorist financing activity.

For instance, while opening a new account and collecting key KYC information, a bank may find through open source record checks that an individual/business had defrauded innocent investors previously, or was part of a global criminal network. This information may hint that this potential client could be an elevated money laundering risk.

Europe:

Over the past few years, there have been several high-profile cases of alleged money laundering. These have increased the attention of the general public and regulators alike. This has subsequently been a result of the penetration of illicit funds and fraud into European societies. Existing AML requirements are continuously adjusted to better prevent such tactics.

The evolution of customer expectations is adding higher imposition on organizations. Delivering seamless, fully digital and mobile experiences is becoming compulsory. The unprecedented situation that has been inflicted by the coronavirus pandemic in 2020 is an added setback. This is also setting new standards on the pace of digital transformation in KYC compliance.

To address these challenges, the EU has introduced a number of more stringent financial regulations over the last few years. This is to potentially tighten the enforcement powers across the bloc. — the European Commission’s Action Plan released in May 2020.

The extensive penetration of money laundering practices can be seen in European societies. News stories such as the Panama and Paradise Papers is critical in this context.

A number of regulations have been mandated to address the general issues. This is done on the basis of the challenges which the financial sector had undergone for the previous ten years. In particular:

The Fourth, Fifth & Sixth Anti-Money Laundering Directive (AMLD4, 5 & 6) are aimed at counteracting the extensive penetration of money laundering in the societies. This can be done by introducing more thorough checks. Moreover, better cooperation between countries, as well as harsher criminal liabilities are crucial.

The Payments Services Directive (PSD2) entices customer-centric innovation in the banking world. The focus is on preventing payment fraud and misuse of electronic financial tools;

The updated Markets in Financial Instruments Directive (MiFID II) is another important regulation. It is driven by the necessity for more transparency in financial investment operations;

The General Data Protection Regulation (GDPR) was the EU’s response to the general public’s request. It was passed to regain control over personal data and identity.

KYC Methods In CASA For Banks

For framing KYC policies, banks must follow the RBI guidelines. Every bank, has to consider the following major aspects:

a) Customer Acceptance Policy–

To make sure that explicit guidelines are applicable to the acceptance of customers.

b) Customer Identification Procedures–

To efficiently identify the customer. This helps to verify his/her identity. This can be done with reliable, independent methods of documents, data or information.

c) Monitoring of Transactions– This policy observes the standard activity of the customer. It can then mark transactions that fall outside the regular pattern of activity.

d) Risk management– Establish appropriate protocols as well as implicate their effective implementation.

As part of the Know Your Customer policy, a Customer/user may be defined as:

A person or entity that possesses an account and/or maintains a business relationship with the banking institution

The person on whose behalf the account is maintained (i.e. the beneficial owner)

Beneficiaries of transactions which are carried out by professional intermediaries. These can be stockbrokers, Chartered Accountants, or solicitors etc.

Any person or entity involved with a suspicious financial transaction. This can have significant impact on reputation or other risks to the banking institution. For instance, a wire transfer or issue of a high-value demand draft as a single transaction.

Going paperless — Digital KYC verification

The immediate benefit of a paperless form of KYC is the decreased costs for performing KYC. Video KYC brings in the additional benefit of being completely remote. This is because digital KYC still requires a visit either to the customer’s doorstep or a touch point.

Video KYC in particular thus presents a significant advantage for achieving scale. It has become a crucial factor in the success of fintech initiatives for financial inclusion. This is primarily because it delivers a cheaper method for achieving compliance even in remote locations.

Several fintech companies have introduced new-age digital identity and authentication technologies. They serve the purpose of KYC compliance. These utilize Artificial Intelligence, Blockchain and cloud-based API technology, among many others. Some of these have already been applied in other sectors, like the use of digital KYC verification to open mutual fund accounts.

The amount of data and related analysis projects a scope for new ways in which the data can be leveraged. Some instances include:

– New age risk mapping

– Using machine learning for false positive screening

– Using robotics for dealing with huge volumes of content and unstructured data

The scope for innovation has huge potential. It is a primary reason why the RBI’s regulatory sandbox has specified a focus on digital KYC technology. For starters, the Reserve Bank Of India should mandate digital KYC to become remote as well.

In the US, KYC started with the introduction of the Banking Secrecy Act (BSA) in 1970. This act was developed to control drug trafficking by keeping an eye on black money transactions. Subsequent AML regulations were developed on the basis of BSA in 2001 in the form of the USA Patriot Act which was implemented in 2003.

Later, following BSA, many other regulators introduced KYC and AML Regulations. This was done on regional and international levels.

Digitization of KYC — Major Amendments In Banking Regulations

As a measure to implement digital KYC verification, the finance ministry as well as RBI has introduced several amendments over the last 2 years. The Reserve Bank of India (RBI) acts as the regulatory authority for banking in India. The amendments also ensure that digital KYC verification meets regulatory requirements.

In May 2019, RBI announced important amendments to the Master Direction on KYC. This included updating its list of documents eligible for the identification of individuals. The KYC details apply to banks and other regulated entities. It helps them understand their customers and their financial transactions better. This, in turn, helps them better manage their risks. As per the RBI notification. banks can carry out Aadhaar authentication/offline-verification of an individual. This can be done only when he/she voluntarily utilizes his/her Aadhaar number as ID.

The Ministry of Finance (Department of Revenue) has introduced digital KYC by amending the Prevention of Money-laundering (Maintenance of Records) Rules, 2005. It said in a gazette notification dated 19 August 2019. Digital KYC means capturing live photo of the client. It also captured officially valid documents. It also permits capture of Aadhaar for offline KYC verification. (To know more about the offline KYC rules, click here )

In January of 2020, RBI amended the KYC norms allowing banks and other lending institutions to use VideoKYC. This move will help them onboard customers remotely. VideoKYC, which will be consent-based, will make it easier for banks and other regulated entities to adhere to the RBI’s KYC norms. (To know more about VideoKYC norms, click here )

Regulatory Authorities Around the Globe for KYC

The following highlights the major regulators around the world. They develop, recommend and implement KYC and AML compliance around the world:

FATF (Financial Action Task Force) is a global authority. It gathers and analyzes money laundering and terrorist financing data from across the globe. It gives regulatory guidelines based on its findings. It has 190 member countries.

FinCEN (Financial Crimes Enforcement Network) is a bureau of the USA treasury department. It collects the financial transactions data. It uses this data for financial crime mitigation and international level.

FINTRAC (Financial Transactions and Report Analysis Center) is a regulatory authority in Canada. It analyzes the financial crime data and works on the detailed implementation of KYC and AML rules in Canada.

FINMA is a financial regulatory authority in Switzerland. It oversees banks, insurance companies, stock exchanges, etc. The authority oversees KYC/AML regulations. This applies to all the institutions liable for regulatory compliance.

Europol is a EU authority that works on anti-money laundering and mitigation of financial crimes like terrorist financing.

Major updates in Global KYC/AML Laws

Amendments in Canada’s PCMLTFA rules

Canada introduced changes to its KYC and AML regimes to collaborate with the global regulations of FATF. It amended its PCMLTFA rules. FinTRAC, is responsible for the nationwide implementation of these rules. Digital KYC will be conducted in the manner of scanned copies of documents that can be used for KYC verification of the customers.

The USA expanding its Counter-Terrorism Powers

The USA has transformed its KYC rules to combat increasing money laundering and terrorist financing. It expanded its counter-terrorism powers. It now targets international financial institutions around the world. These culprits are responsible for aiding the terrorist groups working in the U.S. Recently it filtered three Korean groups. These are namely, Bluenoroff, Lazarus Group, and Andriel. They were responsible for the global cyber attacks on financial institutions.

UK MLA Amendments

The UK introduced amendments to its KYC and AML regulations to expand on an international level. The Money laundering Act (MLA-2017) allowed UK-based businesses to practice the MLA rules in their international affiliates.

The EU 5AMLD and 6AMLD

The EU introduced its Fifth Anti Money Laundering Directive (5AMLD) in 2018–19. 5AMLD limited the transaction and deposit limit on the prepaid cards. If the card holder will deposit or make a transaction of above EUR 150 the prepaid card provider will have to run KYC and AML on its customers. The amount is EUR 50 for online transactions.

6AMLD is an improved endeavour to normalize AML/CFT regulations in the EU region. 22 predicate offences are provided in the official journal of 6AMLD.

FINMA gave banking certificates to Crypto Banks

FINMA and Swiss regulatory authority issued banking certificates to pure-play cryptocurrency banks. Tight KYC and AML regulations are imposed on these banks.

Real KYC & VideoKYC For CASA

At Signzy, we have developed 2 proprietary Digital KYC products. They offer the perfect solution for onboarding savings and current accounts — Real KYC & VideoKYC. Here are some benefits:

‘Free of Cost’ Process: RealKYC verification is not liable to charge any extra amount to the customer. A company or institution may need to pay automation costs of installing verification systems for the long-run.

Faster processing: The RealKYC service is an automated online process. This implies that KYC information can be transferred in real-time and does not require any manual intervention. The paper-based KYC process can be delayed for days and go up to weeks to get verified. Using the RealKYC process reduces this to just a few minutes to verify and issue.

Account opening in less than 2 minutes: Signzy’s VideoKYC product is capable of onboarding a new CASA account in less than 2 minutes.

End-to-end encryption for VideoKYC: This feature makes all calls made to officials for verification secure, with zero chance of your data being compromised.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

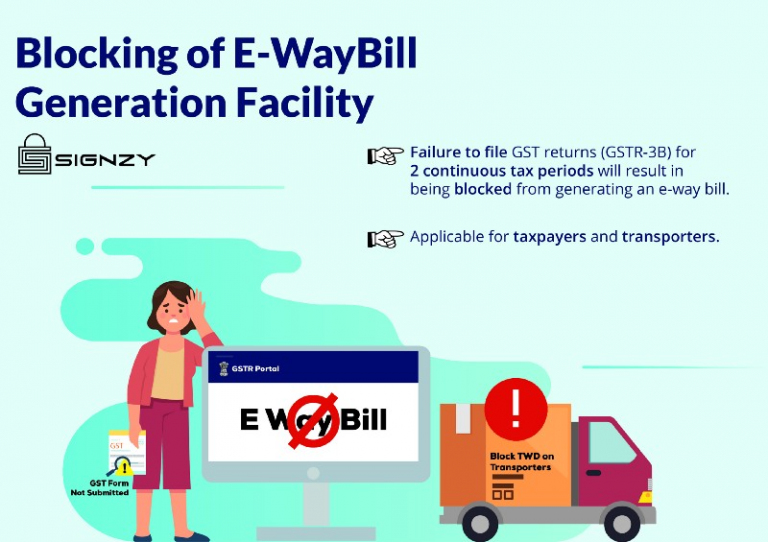

The Indian government has introduced new regulations to control the E-Way bill(EWB) generation facility. This move will identify and penalize GST non-filers and evaders. With effect from December 2, 2019, the blocking and unblocking of the EWB generation facility has been implemented on the e-way bill portal.

EWB generation has been deactivated for taxpayers who haven’t filed their returns for the previous two months. In this regard, Form GSTR3B is to be considered (which is filed by normal taxpayers) for the blocking of E-Way Bill Generation. The move is in accordance with Notification #74 which was released on 31st December 2018 to include Subrule ’E’ under Rule 138 of the GST Act.

What is the objective behind blocking e-way bill generation for taxpayers?

According to a report by Economic Times based on GSTN data, around 20.75 lakh GSTINs have not filed their GSTR-3B for September and October months. Moreover, around 3.47 lakh GSTINs (16.7%) of these had transactions for September and October 2019 in the e-way bill system. Taking under consideration the increase in the number of tax defaulters, their ability to generate E-way bill had to be blocked. The tax department is of the opinion that non-filing of returns has been the primary reason for the decline in the GST revenue collection so far.

Blocking of E-Way Bill Generation Facility

Every taxpayer who is registered under GST is required to file GSTR-3B, on a monthly basis. GSTR-3B includes details of sales and purchases made by a business and the final tax payable after claiming input credit.

As per the new rule, when a taxpayer fails to file his or her GST returns (GSTR-3B) for two continuous tax periods, he or she will get blocked from generating an e-way bill. A blocked GSTIN cannot be used for generating an e-way bill. This applies to both consignor or consignee. For example, if a taxpayer failed to file his/her GSTR-3B returns for the months of September and October 2019, his/her E-way bill generation facility would be blocked effective from 2 December 2019.

The new rule also applies to the transporter who will be unable to generate EWB using the blocked GSTIN of the taxpayer.

The blocking of EWB generation will not impact previously generated EWBs in any way.

Unblocking Of E-Way Bill Generation Facility

Unblocking of e-way bill generation facility restores the facility of generation of E-Way Bill. In the event of filing of the return for the default period(s), the default period is reduced to less than 2 consecutive tax periods. This is in respect of such taxpayers GSTIN (as Consignor or Consignee),

For updation of his/her status the taxpayer can visit the EWB portal. Select the option ‘Search <Update Block Status’. Enter their GSTIN and use the Update Option to get themselves unblocked on GST portal. This applies only when GSTR-3B return has already been filed for the default period(s).

EWB generation facility can also be restored by the jurisdictional tax official. This can be done on the basis of manual representation by a taxpayer. The tax officials will issue an online order on the GST Portal, for accepting or rejecting such requests of the taxpayers. In case he accepts the request, the facility will get restored.

Taxpayers will usually receive an Email/SMS of acceptance or rejection will be sent to taxpayer on email ID/mobile number. In order to view the status of the order issued by the tax official,taxpayers can login to the GST Portal. Using their GSTIN, the user can go to Dashboard>Services>User Services> View Additional Notices/Orders.

The Unblocking of EWB will be valid till the period indicated by the tax official in his/her order. The GST Portal will send a reminder to the taxpayer about 7 days before the expiry date via mail/SMS.

Impact Of Blocking/Unblocking EWB Generation On Transporters

Transporters who are enrolled on the EWB portal but not registered on GST portal will not be impacted in any way. This is because they are not required to file GTR3B returns.

If the GSTIN of the transporter registered under GST portal is blocked, that GSTIN cannot be used. This rule applies to Consignor, Consignee or transporter while generating EWB or updating transporter details.

In case an EWB was generated before blocking, the transporter can also update the vehicle and transporter details. He/she can carry out the extension in validity period of these EWBs if required.

Impact On Taxpayers Who Are Blocked From EWB Generation

Not generating an e-way bill will be considered as an act of non-compliance as per the provisions of the GST law. In such a case, the business may be prevented from delivering goods without an e-way bill.

When goods are transported without an e-way bill, the authorities can claim that the consignor of the goods has made an attempt to evade taxes. A subsequent levy a fine equal to the tax amount is payable in such case. Such commodities and the vehicle transporting them can be seized or detained. Both the goods and the vehicle may be released upon successful payment of the pending tax amount and the penalty mentioned by the concerned officer.

The absence of an e-way bill during transportation of goods can lead to the disruption in the day-to-day operations. It can also hamper delivery of goods for a business. This move by the government is intended to push taxpayers to be more compliant and make sure they file their returns/make their tax payments on time.

Businesses need to approach with caution by filing their GSTR-3B within the deadline. Doing so ensures that there is no disruption in their business-related operations. This new modification to the e-way bill system may effectively improve GST revenue collection.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Digital KYC, with its innovative approach to customer verification, is ushering in a new era for credit card onboarding. By marrying state-of-the-art technology with traditional Know Your Customer procedures, it promises a more efficient, rapid, and secure experience for both financial institutions and their customers. This transformative tool not only optimizes the application and approval processes but also bolsters trust and regulatory compliance. As we venture further into the digital age, the profound influence of Digital KYC on reshaping the credit card landscape becomes ever more apparent. Join us in exploring this remarkable shift in the financial sector.

The financial services marketplace is extremely competitive. As such, acquiring new credit card customers is never easy. The task of successful customer onboarding is often even tougher. Many documents around company credentials and financial statements need verification. The KYC onboarding process is required to meet complex regulatory requirements.

The nature of the documents required for KYC onboarding of a new credit card application can be complex. This often leads to interactions between the sales teams and the customer. Getting the correct documents to complete the KYC onboarding often causes unexpected delays. This leads to poor customer experience and a loss of revenue for the company. Another important aspect is a lack of digital automation in the KYC onboarding process. This leads to longer onboarding cycle times. The resulting delays negatively impact customer experience. The subsequent outcome is a loss of revenue for the card company. This is because customers cannot be charged until they start using their cards.

Challenges For Customer Onboarding For Credit Card Applications

An article by FintechFutures highlights the Forrester Consulting survey. It predicts that on average, clients are contacted ten times during the KYC onboarding process. The clients are asked to submit between five and up to a hundred documents. Also, it costs up to $25,000 per client, with the average cost calculated at $6,000 per new client. The following are the challenges of the current process:

The lack of structured process

KYC onboarding needs to follow different processes. This can be across departments such as credit, legal and operational. The tricky part is that every compliance officer (or compliance department) might have their own interpretation of regulations. Thus, they end up having their own process specific to their own department/entity within the bank. It also means that they will have three different interpretations of regulations/processes. Moreover, customers are likely to get confused on why they need to provide the same information at several points of the process. This information can be duplicated in nature for several different parties.

Changing regulations

In today’s world, KYC regulations are changing on a monthly or weekly basis. Hence, banks need to adapt their systems accordingly. They need time to explain to the client why new changes are happening. They must also ensure that the changes are amended in the KYC digital onboarding process. Due to endless regulations, banks need to re-visit current operations/processes. They must now rely on new technology initiatives. For ex: process reengineering, digital transformation etc to make themselves compliant.

Culture

Financial institutions always tend to have a close relationship with their clients. Underinvestment in strategic opportunities (such as KYC onboarding) is still missing. This is along with the drive to understand customers changing needs and market dynamics. McKinsey conducted a recent survey among the global executives across the world. In the report, culture accounts for 33% among the most significant barriers to digital effectiveness.

Access

With modern technology, banks are getting increasing pressure to do everything on a real-time basis. For example, a customer expects that everything needs to be available on mobile. This can help them avoid visiting the branch and accessing the app from anywhere at any point. Modern banks are still using legacy systems. This leads to a challenge in providing customers with an end-to-end digital experience. With advancements like robotic process automation (RPA), banks can easily overcome this hurdle.

Time-consuming processes

The entire process of KYC onboarding can be very time-consuming. This is due to the vast number of documents needed, multiple touch points and departments involved in the process. Also, it changes for every entity within an organization. For example, a bank has three different entities: corporate, retail and insurance businesses. These can cater to different types of businesses/customers.

Quality

As per PwC, the remediation exercise of the customer has shown that due diligence process varies from each and every entity, from country to country. Thus, the quality of the experience can vary to a very large extent within one financial services entity. So if a customer visits the same bank in Singapore and India, their KYC onboarding experience will vary. I understand a lot of processes are country specific, but that is something which needs to be addressed.

The Need For Speed In Digital Onboarding

Onboarding digital banking customers is a real pain point for banks offering credit cards. This affects user experience by a great deal. Banks heavily invest in attracting new customers. They also talk to existing clients for additional facilities. The challenge here is that with product application workflows are slow and complicated. Another factor is that a poor KYC onboarding process can seriously undermine these efforts.

According to a Marketforce survey, onboarding a new customer takes less than 10 minutes at 32% of incumbent banks. However, it still requires more than 24 hours at 19% of financial institutions.

Almost 39% of respondents can’t even onboard entirely on digital channels.

An astonishing 40% of banking consumers abandon their application, according to a survey by Signicat.

Approximately 39% give up because the process drags on too long, while 34% drop off because too much personal information is required.

This calls for an efficient, digital KYC onboarding which not only provides efficiency, but also speed. Simply taking the process online is not the only contributing factor to this. Most customers require an experience like Netflix or Uber — where efficiency as well as time coalesce.

Fighting Frauds With Digital KYC onboarding

E-commerce fraud is becoming more and more widespread and sophisticated. It is a concern for online retailers around the globe. This risk exists because it can be difficult to verify the identity of who is using the card in an online setting. Asking for the card security codes (the 3–4 digit code features on the back of credit and debit cards) is a good preventative measure. Unfortunately, it isn’t always enough.

In a survey by Experian, 63% of US businesses reported fraudulent losses in 2018.

Reports from Juniper Research that online retailers are set to lose an estimated $130 billion between 2018 and 2023 in digital card-not-present (CNP) fraud.

A study by Javelin Strategy & Research in 2018 showed that CNP fraud is 81% more likely to occur than “card-present” in-store credit card fraud.

In its most general terms, credit card fraud refers to a fraudster making a transaction with an online business. This can be done through illicit means mostly by:

Stolen credit card information

Stolen ID

Fake credit card details

The preferred and most convenient way to prevent this is KYC. Many banks, insurance companies, and other types of financial institutions have a KYC onboarding procedure in place. This ensures that their customers and clients are who they say they are. It also helps these institutions to get to know their customers. The companies can also verify whether clients are involved in any illegal activities. Ex: money laundering or bribery.

Implementing the KYC onboarding process stops online fraud before it can happen. It typically involves providing one or more documents to the institution that confirms their identity. These documents can include:

Government ID

Drivers License

Passport

Aadhaar Card

In addition, KYC verification compares the collected data against several AM/CFT databases. It also conducts checks for forged documents and bogus information. This makes KYC onboarding the perfect tool for combating frauds.

Make The Plastic Fantastic — Digitizing The Credit Card Application process

Competition is fierce when it comes to credit card issuing. Many of the traditional approaches to differentiation are losing effectiveness. Interest rates have evened out across cards. Large issuers continue to capture a bigger share of transactions. However smaller issuers are gaining market share in outstandings by bringing portfolios back in house and developing highly targeted customer-management campaigns.

From customer acquisition to onboarding to payments, the digital channel is becoming the most effective way to engage cardholders. It enables issuers to enhance the customer experience. It also helps set the stage for the use of big data and advanced analytics techniques. This can help improve decision making.

McKinsey research highlights that clients are willing to engage digitally, and often start their journey via digital channels.

More than 80% of US-based customers research credit cards online before acquisition.

More than 25% customers get personal recommendations via social networks to keep them updated on purchase decisions.

About 28% of credit card sales are made through digital channels, and two-thirds of the clients activate their new cards online.

Two major areas to be covered for digitizing customer experience are:

Customer acquisition, which specifically involves converting clients from consideration to the application phase. It includes getting them through the approval process in the real-time digital surroundings.

Customer onboarding after an application for a credit card is approved. From the customer’s point of view, the days that follow are either full of pain points or lacking in any kind of contact with the issuer that might help cement the new relationship.

Digital KYC Onboarding for Credit Card Application Process — The Game Changer

The first step in building a relationship with a new client is enhancing the application procedureto be simple, seamless, and quick. The fewer the fields to complete, the faster the application. For example, applicants can enter their demographic information via their smartphone camera. This can be used for verification through facial recognition. Some issuers have managed to cut completion times by up to a third. They have also raised completion rates by more than a quarter. In addition, an increase in digital applications by 40% is acheived by simplifying the application process.

The second step involves engaging new clients so they use their card early and often so that usage becomes a habit. For example, In India, most credit cards require holders to spend a particular denomination in the first 90 days to qualify for reward miles. An analysis by McKinsey shows that the long-term value of a client is up to 3x greater when they are engaged frequently in the first 90 days. However, many issuers assign only about a fifth of their marketing budget to this critical time period.

CoronaVirus Crisis — Issuing Credit Cards Online

From the start of the Covid-19 lockdown, loan and card issuers have come to a grinding halt. This is mainly because both require representatives to visit the applicant for paperwork. The resultant decline in business has forced lenders and card issuers to focus on digital lending.

There are plans in motion for users to issue credit cards while sitting at home, with zero paperwork. On approval, the funds will be credited directly into your bank account or the card will be sent to your address.

According to Livemint, the intermediaries, banks and other financial institutions are requesting the regulator and the government to encourage banks to use the Central KYC (CKYC) and Aadhaar-based KYC.

There are also talks of VideoKYC being used for digitizing issuance of credit cards. As per the RBI notification, when lenders are doing V-CIP, an official needs to be present on the other end for verification. The client has to furnish documents to the official over the video during the procedure. Also, it’s a real-time process that needs to be recorded and stored. Further, the online process eliminates the requirement of physical signature. The same process can be applicable for card issuance.

The New Age KYC Technology By Signzy

Signzy offers a unique AI-based electronic KYC solution called RealKYC. It is a comprehensive suite of micro-services that offers smooth onboarding of new applications for credit cards. It also offers risk management and fraud mitigation.

Signzy has also launched its unique VideoKYC solution for real-time verification. This can be done remotely. VideoKYC strictly maintains compliance with RBI and SEBI guidelines. It is a secure, hassle-free tool for onboarding.

Here are 3 major benefits that RealKYC :

Hassle-Free Application Approval: When a new application is received for a credit card, it has to be approved by several officials. It undergoes severe scrutiny before the application moves to the back end for processing. With RealKYC, there is no need for back and forth. This is because multiple checks can be performed by officials simultaneously. This makes the process efficient and hassle-free.

Credit Checks: Signzy’s unique set of APIs perform comprehensive credit checks against the applicant. This is done to check for worthiness, past default details and so on. which could lead to potential credit risks if the applicant is approved.

Background Checks: Real KYC performs in-depth background checks of the credit card applicant. This may include cross-referencing the applicant against multiple AML/CFT databases, negative checks against registered court cases, etc.

Real-Time PAN verification with VideoKYC; Signzy’s VideoKYC solution offers real-time PAN verification. This helps authenticate the originality of the document. It also conducts background credit checks against the PAN number.

No Photocopies: With VideoKYC, just show the original ID proof and the official on call can take the snapshot as part of KYC proof.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The onboarding process for Asset Management Companies (AMCs) is among the most complex of all client-facing activities. Reams of documentation are exchanged between a client and the investment management firm. It is then distributed throughout the organization. Most of this requires approvals, signatures, and validations.

Digital onboarding requires finalizing legal agreements, Know Your Customer (KYC) and Anti Money Laundering (AML) activities. It also involves opening client accounts on multiple systems and transitioning incoming assets. Each of these activities engages multiple groups throughout the organization. Examples include client service, legal, compliance, and operations. Without well-defined and coordinated procedures, this could lead to errors. Ex: misplaced information, breakdowns in communication, and duplicated efforts are likely. The right-hand needs to know what the left hand is doing in order to properly manage all the hand-offs and moving parts.

Benefits of improving onboarding:-

Ability to generate fees sooner.

Increased potential to cross-sell, additional products, and services.

More referrals from clients due to a positive experience.

Reduced client turnover.

More efficient resource allocation.

Better views into process status.

Fewer mishandled communications and handoffs between the team.

Measurable efficiency through metrics.

Faster addition of new products and services.

Why Digital KYC? The Need For Digitization Of KYC In Mutual Funds

At present, investing in a mutual fund requires a second round of KYC. This is also true even for customers who have completed KYC in their bank accounts. The procedure involves the submission of identification and address proofs along with photographs. The distributor or adviser must physically meet the customer to conduct ‘in-person verification’ for him/her. This requirement greatly hampers the growth of mutual funds online.

It also affects access to mutual fund investments for those in remote areas. In 2019, the Nilekani committee proposed that there should be a simple KYC procedure for opening a mutual fund account funded from a KYC-verified bank account. However, inflows into such a folio and redemptions to it must be restricted to this account.

This leads to the digitization of KYC. Among the many advantages of getting paperless KYC done, the following benefits are most important:

Personal Details are Secure: All information is stored and transmitted on the website with a special configuration. Whether it is your Account Information, Demographic Data, Biometric Data, etc. The KRA, Fund House, or AMC’s Portal is maintained with the highest level of Security. It reduces illegal activities of money laundering, loan scams, identity theft, and fraud.

You are the Boss: The option to invest will always be yours. The digital KYC mechanism is completely dependent on your decision. Not only that, you have the choice of providing access to your details to whomsoever you want. In some cases, if you change your mind. You may not want to invest in Mutual Funds. Whereas, if you opt for offline KYC. It is possible that your self-attested documents end up with unauthorized parties. This risk gets reduced to a large extent by taking the online KYC mode.

Instant Process: No Human element is involved that means no Red Tape is involved. The efficiency in the digital process ensures no delays. Comparatively, the offline process would take at least a few days.

Transparency: Incidents of the KYC documents in illegal and illegitimate persons occurred commonly. Opting for Online KYC, you can avoid such an event. The websites store the data in encrypted servers. It makes the possibility of a breach highly unlikely. Besides, the trespasser or the source of the breach can be traced in online transactions. They can be brought to legal authority with proof.

No Hidden Costs: Some Mutual Funds agents may charge extra amount as KYC Registration fees. And investors need to pay to avoid the hassle of taking time off from work and visiting the Government Agency in person. With eKYC, you do not need to pay in addition to the investment amount.

Compliance: Your data gets validated using the latest technologies. This increases the overall security of the system. It also ensures that the digitally transferred document is legally valid.

The Road To Digitization Of KYC

As per regulatory developments from January 1, 2011, KYC is mandatory for investors wanting to transact in Mutual Funds. This is regardless of the transaction amount. It implies that you will not be able to process any fresh MF purchases post January 1, 2011. This is true except when you are MF KYC compliant as per CDSL Ventures Limited (CVL) norms.

This implies that you can always ask your broker to provide you forms for submission to your KYC. Since there are no charges for mutual funds they may not be useful. As such, it is better you also understand you can get your KYC done. Follow these steps:

1. Get the Form

The KYC application form can be availed from the investor service centers for the particular Fund, CAMS or at any specified ‘Points of Service’ (POS) of CDSL Ventures Ltd. You can also download it from your broker, advisor or AMC.

2. Documents

The following lists the set of documents which are required for submission with the KYC application form:

1. A recent passport size photograph

2. PAN card copy

3. Address proof (Recent bank statement will work but if you have to get your bank statement in the email you need to visit your bank branch to get an original one.)

The document submission can be done at the CAMS Online office in your city. Ensure you carry the originals along with a photocopy of the documents because at times they might need to verify with the originals.

3. Verification

Once the KYC application form and supporting documents are verified, the investors will receive a letter authenticating their KYC compliance. They normally give you the letter in a few hours to a max of 24 hours for this identity verification api .

You can verify your KYC status online. You should verify on the day of form submission that your status is processing. Once it is done, your status should change to VERIFIED.

Actually KYC need not be done at your broker’s end. But some online systems do not accept the order. This can happen if they don’t have the data in their own system and so it is better to get that done as well.

KRA and K-IPV In KYC Collection

SEBI had initiated the usage of uniform KYC by all SEBI registered intermediaries (RIs). This was done to bring uniformity in the KYC requirements for the securities markets. In this regard, SEBI had issued the SEBI KYC Registration Agency (KRA), Regulations, 2011.

KRA is the authority for the centralization of all KYC records and details in the securities market. The client who wishes to open an account with a broker shall submit the KYC details. They can be submitted through the KYC Registration form with supporting documents. The Intermediary is responsible for conducting the initial KYC. The RI should also upload the details to the KRA system. The KYC details are accessible to all SEBI RIs for the same client. So once the client has undergone KYC with an RI, it is not necessary to repeat the same process again with other RIs.

It is compulsory for each client to be registered with any one of the various KRA registered intermediaries. This should be done before availing the benefits of any intermediary. Such benefits include Stock Broker, Mutual Fund Companies, Depository Participant, Portfolio Management Services (PMS) etc.

In-Person Verification (IPV) is part of the process of doing KRA-KYC registration of clients. KRA compliant clients are not required to undergo this process.

Importance Of IPV

The Prevention of Money Laundering Act, 2002 (PMLA), came into effect from 1 July 2005. The Act enforces that no one could use investment tools to hide their illegal wealth. Soon after, SEBI mandated that all intermediaries should adopt the KYC policy. It was also necessary to plan and install certain policies. The policies should follow vis-a-vis the guidelines on anti-money laundering measures.

Since 1 January 2011, KYC compliance has been made mandatory for all investors. This is irrespective of the amount invested and includes the following transactions:

a. New / Additional Purchases

b. Switching Transactions

c. First-time Registrations for SIP/ STP/ Flex STP/ FlexIndex/ DTP

d. Any SIP/STP/trigger-related products which were introduced after the enactment of the act

e-KYC (Know Your Customer) is a value-added feature that is offered by many financial institutions. E-kyc is useful for making the application process convenient. Investors can access it and upload the necessary documents. It can be done from the comfort of their home or office. As previously discussed, this is applicable to only SEBI-approved KRAs. For ex: CVL and CAMS can complete the e-KYC process. This means that Digital KYC can be used for IPV as well.

EKYC — The Miracle Turned Myth

To remove the repetitive submission of documents, SEBI launched the concept of common KYC in 2011. With this move, the first intermediary processes the KYC-related information and sends them to the KYC Registration Agency (KRA). Once your account is created, any other intermediary can make use of the same details in the future for new accounts.

Why eKYC?

The concept of common KYC smoothened things for retail investors, However, it was still a time-consuming process (8–10 days). It also included the problem of in-person verification. This also increased the cost of servicing small investors while preventing immediate on-boarding of new customers.

SEBI launched eKYC in order to make the procedure more investor-friendly. It enabled customers to verify their identity and upload documents digitally. To get started, you only needed to quote your Aadhaar number, PAN number, e-mail id, and mobile number. Once you type in the details, you will receive a one-time password (OTP) in your Aadhaar-registered mobile number. After entering the OTP, the eKYC process would be completed and you could start investing in mutual funds within minutes.

While Aadhaar based eKYC had been introduced as a means for onboarding, there were a lot of discrepancies. This was especially after the Supreme court judgement on the use of Aadhaar based eKYC. It was later reintroduced. This had left a state of confusion and many AMCs continued traditional methods of KYC collection for onboarding. Physical KYCs are more time-consuming. The distributor has to submit the documents to KYC Registration Agencies or KRAs. The KRA nodal agencies have to manually fill in the data in their systems from the applications. If the handwriting is illegible, capturing the KYC data could lead to errors. This would delay the process further.

The SEBI Way Of Digital KYC

In a recent move on April 24, 2020, the Securities & Exchange Board Of India (SEBI) has issued the latest guidelines on the digitization of the KYC process. Some of the highlights are mentioned below:

1. Know Your Customer (KYC) and Customer Due Diligence (CDD) policies form a part of KYC. They are the foundations of an effective Anti-Money Laundering process. The KYC process requires every SEBI registered intermediary (also known as ‘RI’) to collect and verify the Proof of Identity (PoI) and Proof of Address (PoA) from the investor.

2. The provisions as laid down under the Prevention of Money-Laundering Act, 2002, Prevention of Money-Laundering (Maintenance of Records) Rules, 2005, SEBI Master Circular on Anti Money Laundering (AML) dated October 15, 2019 and relevant KYC / AML circulars issued from time to time shall continue to remain applicable. Further, the SEBI registered intermediary will continue to ensure to obtain the express consent of the investor. This should be done before undertaking online KYC.

3. SEBI, from time to time has issued various circulars to simplify the process of KYC by investors / RIs. Constant technology evolution has led to multiple innovative platforms being created. These allow investors to complete the KYC process online. SEBI held discussions with various market participants and based on their feedback, technology like Aadhar-based e-Sign service which can facilitate online KYC will now be used. This is done with a view to allow ease of doing business in the securities market.

4. New regulations allow Investor’s KYC to be completed through an online / App-based KYC. There is also provision for in-person verification through video, online submission of Officially Valid Document (OVD) / other documents under eSign. It allows the introduction of VideoKYC, which was also allowed by RBI for the banking sector earlier this year. (Click here<

to read more about RBI Guidelines for VideoKYC)

5. SEBI registered intermediary may implement their own Application (App) for undertaking online KYC of investors. The App shall facilitate taking photographs, scanning, acceptance of OVD through Digilocker, video capturing in a live environment, usage of the App only by authorized persons of the RI.

6. The guidelines also allow RIs to undertake the VIPV(Video In-Person Verification) of an individual investor through their App. This is done to ease investor onboarding.

Digital KYC For The New Era

Signzy has developed an AI-based electronic KYC solution called RealKYC. It consists of a host of microservices that provide the following benefits to AMCs

Reduction of TAT: During investor onboarding, the traditional method of KYC collection involves the submission of a lot of documents and processing that is done by several departments and their officers. This can be a time-consuming process but with VideoKYC, the entire process is automated and can be done in a matter of minutes in real-time.

Lower Operational Costs: The onboarding process for a new investor can require several checkpoints that are cost-effective. There is significant manpower involved as well which also raises the cost of onboarding. All these factors can be automated with RealKYC, thereby reducing operational expenses.

Remote Onboarding: With RealKYC, there is no need for investors/entities to pay multiple visits to the physical branch for the processing of KYC. They can simply visit the website and submit all their documents as well as get the verification done, online.

Signzy’s VideoKYC solution offers a simple, secure KYC collection process that is 100% compliant with the latest SEBI Guidelines. The benefits include:

Compatibility With Most User Devices: This solution has matured over dialects, browsers and low-internet scenarios. This means that most users can undergo VideoKYC without any technical pain points.

Improved BackOps; Our Patented AI reduces 90% Backops effort, making onboarding of investors a smooth process.

Conclusion

KYC or Know Your Customer is a compulsory requirement for those wishing to invest in Mutual Funds. It is mandatorily needed by the Market Regulator SEBI (Securities and Exchange Board of India). This identification process needs to be undertaken only once. KYC was introduced to avoid fraudulent activities. eKYC for Mutual Fund was launched for the ease of investors.Digitization of KYC merely changes the mode of KYC collection and not the process.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The politics of data protection can be seen through three lenses. That of the government, the individual, and private companies. The concerns of all three have to be addressed to devise an effective data regulation framework. For the government, pressure is mounting to safeguard citizens’ personal data. However, it is their prerogative to preserve national security. This may require access to personal data to combat illegal activities like trafficking. Companies are grappling to strike a balance between compliance, personalization and interoperability. It then becomes the data regulator’s responsibility to safeguard personal data. But, without risking national security or hampering innovation and economic growth.

The Indian Personal Data Protection Bill (PDP) of 2019 is on the verge of becoming a law. So, questions on it’s power and compliance are at the fore. This blog addresses prominent questions on the bill in the global & national context:

Would PDP compliance result in GDPR (General Data Protection Regulation of the European Union) violation?

Does the bill itself threaten global cybersecurity?

Will government mission creep grow as a side effect?

Is innovation stagnancy a real possibility stemming from the bill?

A preliminary understanding of the data protection regulations in place in the EU and India is helpful. You can take a look at our article comparing the GDPR and PDP Bill.

Will complying with India’s PDP Bill mean violating the GDPR?

The intent of the regulations is identical. Both were created to safeguard data and privacy. But, their criteria for compliance is not. This means that if a company’s operation is compliant to the GDPR, it won’t necessarily be PDP compliant. To remain compliant the data fiduciaries will have to chart their course according to the standards of each framework. Both regulations have different requirements and prerequisites. The question is if compliance to any provision in the PDP is contradictory to the needs of the GDPR.

Many obligations overlap or are at different degrees on the same spectrum. But, the International Association of Privacy Professionals (IAPP) points out a problem. Indian companies may find themselves at a crossroads when processing data under the purview of the GDPR. If the data they collected was only on the basis of “contractual performance”.

This is one of the lawful bases that permits an entity to process data under the GDPR. The PDP does not list “contractual necessity” as a legal basis for processing. This is why the confusion arises. Many businesses in the online services environment heavily rely on this criteria to process personal data. It allows an entity to transfer data to another entity as a contractual obligation. For example, shipping a product requires the data to be shared with the deliverers and customs officials. Travel agents require the data be shared with the hotel or airlines.

This creates a grey area. Complying with one regulation may make it difficult not to violate the other. This is because swapping the lawful bases (to comply with the PDP) is not allowed under the GDPR.

It can be assumed that the data fiduciaries/ data controllers are not violating the GDPR when they change the lawful basis. Even then it will be a challenge for larger entities. For example: Companies with several foreign subdivisions. They will have to redefine, re-communicate, and re-implement processes. In particular, data collection, usage, & protection protocols for all parties involved in the data flow.

Does the Indian Personal Data Protection Bill threaten global cybersecurity?

PDP proposes banning re-identification of data. Cybersecurity and privacy researchers have revealed that this discourages researchers. They cannot thoroughly investigate security weaknesses, thereby encouraging cybercriminals to exploit them.

But, what is re-identification? First it’s important to define de-identification and its necessity.

When a company processes an individual’s data, algorithms are used to decouple sensitive details from identifying information. For example: medical records and traces of location separated from phone numbers and email addresses . This is de-identification.

Organizations can recover the link between the users’ identities and their data when required. The reverse process is called re-identification. This is a routine practice when done in a controlled environment designed for security by legitimate entities.

The risk is of malicious parties getting their hands on a de-identified database and re-identifying it. Data breaches and leaks are an increasing concern in our data-fied world. The PDP proposes to criminalize the process of re-identification without consent of user data. It’s called illegitimate re-identification. While this seems only logical, it may threaten global cybersecurity.

Researchers often perform meticulous cybersecurity tests and privacy guarantees without knowledge or consent of an organization. They act with public interest in mind and their work makes the digital world a safer place. The blanket ban could hamper research altogether. With risk of penalties and even jail time, security researchers would not partake in this testing for social good. Worse yet, software vendors might be tempted to instigate legal action against such researchers.

At India’s scale, impeding cybersecurity and privacy research could leave the cyber realm at large to malicious forces. This threatens global cybersecurity.

What exceptions are given to the government and what does this mean?

The bill gives the central government the power to exempt its agencies from the purview of this act. The purpose of revoking the regulations are vaguely defined. It can be

In the interest of sovereignty and integrity of India or

To preserve national security

This thereby eliminates the obligations of consent, accountability and transparency to ensure just processing of data. A regulation drafted for the protection of personal data can rid the government it’s duties and result in mission creep. This can give rise to a Big Brother like situation with the government morphing into a surveillance state under the guise of national interest. In the absence of a privacy law, it can be dangerous for the State to have access to all our personal data.

Are there any provisions for companies working on innovative data driven tech?

Companies are preparing to adapt to the new compliance requirements. But, there are growing concerns for tech companies:

Mounting operational expenses

Compliance constraints

Rising cost of doing business

Increase in barriers to entry

This could limit the ability of new competitors to enter the market. Restrictions on sharing data with third parties could make it difficult for companies to collaborate on data-driven innovation.

There is a massive flux of data across borders. Governments are increasingly considering data and digital infrastructure as integral to national security and economic growth. Developing economies in the past wanted to foster domestic auto production. Today, governments are focusing on endeavors to make their domestic tech industries thrive.

Governments are drafting policies on data infrastructure and technology. This includes data localization constraints, and limits on foreign investment on technology. The aim here by this is to foster innovation at a local level. Barriers and constraints have the tendency to prioritize national goals over global innovation. And so it is important to find the right balance between multiple objectives.

As a welcome counter to such provisions, the PDP introduces the concept of a “sandbox”. It gives the Data Protection Authority the power to modify provisions for certain data fiduciaries. Those that work for “innovation in artificial intelligence, machine-learning or any other emerging technology in public interest”. Under Section 40 of the PDP bill exemptions may be given as part of the sandbox. This includes relaxations. Specifying a clear purpose for data processing and collection may be relaxed. The limits to the period of data retention can be revoked.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The data economy can be a Catch-22. It can succumb to corporate surveillance capitalism on the one hand and an authoritarian digital “welfare” state on the other. The European Union (EU) places itself as the alternative to both. Its strategy to regulate technology over the next decade is to set that precedence. Whether it is successful is up for interpretation. On 19th February 2020, the European Commission (executive branch of the European Union) published a 26-page whitepaper on Artificial Intelligence (AI). The paper titled a European Approach to Excellence and Trust states the EC’s intent to regulate and advance AI.

This blog will explore the reach, requirements, and reservations of the guidelines the whitepaper introduces.

Reach: A Risk Barometer Approach

The whitepaper will have consequences for those using and developing AI. To be specific, businesses that are participants of the data economy. It’s drafted to effectively regulate AI while not being dictatorial. Strict measures could create a disproportionate burden for SMEs.

The paper defines AI as

“Systems that display intelligent behavior by analyzing their environment and taking actions — with some degree of autonomy — to achieve specific goals.”

However, the proposed requirements will mainly affect AI which is deemed “high-risk”. This is enumerated by the EC as:

“…deployed in health care, transport, energy and parts of the public sector, or if it is used in the employment sphere (for recruitment puposes or in situations impacting worker’s rights), or for remote biometric identification and other intrusive surveillance technologies.”

Due to this definition and set scope, the suggestions would not apply to advertising technology or consumer privacy. The assumption here is that risk can be finitely calculated. This leaves many contentious issues outside of the purview of the guidelines. For example, data brokers that leverage AI to predict identities and hyper-targeted advertising.

It is anticipated that the new framework will have extraterritorial impact, like the GDPR.

Requirements: The Precursor to Compliance

The AI applications classified as high-risk would be regulated by the following key features. These center on safety, security, fairness and transparency:

Training data The paper reiterates that if there is no data, there is no AI. The decisions and performance of an AI are dependent on the data sets it has been fed and trained on. To ensure that the services or products that the AI system enables are safe, the requirements dictate that it must be trained on a broad enough data set. The training data must also be representation to avoid inadvertent coded discrimination. The data collected to adhere to privacy and data protection standards i.e. the GDPR. (Interested in reading more on the data protection regulations in place in the EU and India? Take a look at our article comparing the GDPR and PDP Bill)

Data and record-keeping Considering the opacity and complexity of many AI systems, certain requirements are put forth to verify compliance. It could allow potentially problematic decisions or actions by the AI to be traced back. The regulatory framework proposes that the following records can be kept: a. Records related to the programming of the algorithm b. Data sets used to train and test the high-risk AI systems (when justified) along with a description of their main characteristic and the reason for their selection c. Documentation on the algorithm and the training methodologies adopted to build, test, and validate the AI

Information to be provided

Apart from the above information, the AI system’s limitations and capabilities must be proactively provided. It should also mention the degree of accuracy to which the system can achieve a specific purpose. This information could be useful to those deploying the AI application. The whitepaper reiterates that citizens should be duly informed when they are interacting with an AI and not a real person. The details should be easy to understand, concise and objective.

Robustness and accuracy Across the AI system’s life cycle, it must correctly reflect its own degree of accuracy. The whitepaper mentions that the outcomes should be reproducible. The AI system must be able to deal with errors and inconsistencies. It should endure overt attacks, and be resilient against manipulated data.

Human oversight The AI system must be ethical and trustworthy. To not undermine human autonomy, the whitepaper insists on the AI being human-centric. This could manifest in different ways depending on the system’s purpose and functioning: a. Output is reviewed and validated by a human before it becomes effective. For example, human intervention needed to approve a person’s KYC. b. Human intervention post the output being effective. For example, reviewing why the AI rejected a credit application, after the decision was put into effect. c. Monitoring the operation of the AI system. This is with the possibility to intervene and stop its functioning in real time. For example, a deactivate button in a driverless car. d. Constraints integrated during the design phase. For example, a driverless car will stop when visibility is low.

Specific requirements (Example: For AI applications used for remote biometric identification)

The application of AI systems for functions such as facial recognition affects the fundamental rights of a citizen. For example the right to a private life and the protection of one’s personal data. Processing of biometric data is to uniquely identify a person. This can only be done in special circumstances with adequate safeguards. The whitepaper declares that the EC will begin a “broad European debate”- on what these circumstances are and their justification.

Reservations: Missing the Mark

The proposed guidelines address issues of personal data protection and pivacy rights, non-discrimination, and cybersecurity. But, it seems to miss the perils of “low-risk” technologies with weakened guidelines.

The whitepaper overlooks that the classification of low risk is not absolute. This could actually be very risky for some. The harms of technology are often amplified to disproportionately affect the marginalized.