The Know Your Client or Know Your Customer (KYC) is a standard process in the investment industry. It ensures investment advisors know detailed information about their clients. This includes risk tolerance, investment knowledge, and financial position. The KYC process conducted during investor onboarding protects the interests of both clients and investment advisors. Clients are protected as their investment advisor knows the best choices for investments. Similarly, investment advisors know what they can and cannot include in the portfolio.

KYC compliance basically revolves around certain necessities and policies. This includes risk management, customer acceptance policies, and transaction monitoring. However, the need for digitizing the KYC collection process is crucial in these times.

KYC in Securities Industry — Rules & Regulations

The Know Your Client (KYC) rule is an ethical requirement of the securities industry. This includes those who interact with customers during investor onboarding and maintaining accounts. There are two rules which were implemented in July 2012 that are applicable in this regard.

1. Financial Industry Regulatory Authority (FINRA) Rule 2090 (Know Your Customer)

2. FINRA Rule 2111 (Suitability)

These rules are designed to protect both the broker-dealer and the customer. The rules provide a mutually beneficial agreement to both parties.

FINRA 2090

The Know Your Customer Rule 2090 cites that every broker-dealer must provide logical effort during investor onboarding and maintaining customer accounts. It is a requirement to maintain records on the demographics of each customer. It is also required to identify each individual who has the capacity to act on the customer’s behalf.

The KYC rule is crucial for the start of a customer-broker journey. It establishes the essential facts of each customer. This has to be done before any recommendations are made. These are required to service the customer’s account effectively. It also provides awareness of any special handling instructions for the account. The broker-dealer needs to be familiar with each person who has the authority to act on behalf of the client. It is necessary to follow all the laws, regulations, and rules of the securities industry.

FINRA 2111

As found in the FINRA Rules of Fair Practices, Rule 2111 goes in tandem with the KYC rule. It covers the topic of making recommendations. Suitability Rule 2111 mandates that a broker-dealer must have sensible grounds on which to make a recommendation. This must be customer-based and depend on the client’s financial situation and needs. This ensures that the broker-dealer has checked the facts and profile of the customer. This must also include the customer’s other securities. This should be done before making any purchase, sale, or exchange of securities.

KYC For Trading/DEMAT Accounts

- Know Your Customer (KYC) is a primary requirement for opening your trading-cum-DEMAT account with a broker. What does KYC mean and why does SEBI mandate KYC for opening a DEMAT account? The perception is that the customer has relevant documentation for online ID verification. It also checks whether the flow of funds have a distinct record through banking channels. Today, it is not possible to activate a DEMAT account without KYC. As per SEBI (Securities and Exchange Board Of India) guidelines, KYC is a must.

- When you open the DEMAT account, the DP / broker will ask you to fill up a KYC form along with your client agreement form. KYC requires basic paperwork and submission of essential documents. It also requires originals for complete verification.

- KYC norms were put out by the RBI in 2002 and have been adopted by SEBI for all investment-related activities. This includes opening a trading account, DEMAT account, mutual fund investments, etc. The idea was to cut down on corrupt practices. Money laundering, acting as fronts for entities, trading in cash without audit trails, fraud, and financing of anti-national activities are some examples.

- With KYC, your data is secure in a central database and the KYC process is applicable only once. After that, it is just picked up from the central database by linking your PAN card.

KYC helps banks and other financial institutions conduct online ID verification and track their customer transaction trails. This helps link all your capital market activity with your bank account. It also assists in tax returns and plugs any gaps in reporting. SEBI has enforced KYC compliance for sectors like mutual fund accounts, DEMAT accounts and trading accounts.

Key steps in the KYC documentation process for DEMAT account

- The first step is the filling of the KYC form if you are a new investor and opening your DEMAT account for the first time. The application forms require demographic information. This can be name, residential address, office address, joint account holder details, account nomination, etc.

- The next step of the investor onboarding process is to present your identity proof. PAN card is mandatory in this regard. You may also be asked to submit an additional government authorized proof. This can be a passport, driving license, voter ID, Aadhaar, etc.

- The third step involves submitting proof of residential address. The document should include the current address in the exact format. You can provide utility bills with link documents. Other documents like bank statements, company letters, etc can also be linked.

- Finally, you must submit a copy of your cancelled cheque. The account holder name must be clearly embossed on the cheque leaf. This is to verify your IFSC code and account details.

This entire process of investor onboarding can be time-consuming as well as heavily dependent on manpower. It also involves a significant amount of paperwork. With the digitization of the KYC process, the complete process has been simplified. Onboarding new DEMAT account holders can now take a matter of minutes.

Know Hows of KRA and K-IPV In KYC Collection

SEBI had initiated the usage of uniform KYC by all SEBI registered intermediaries (RIs). This was done to bring uniformity in the KYC requirements for the securities markets. In this regard, SEBI had issued the SEBI KYC Registration Agency (KRA), Regulations, 2011.

KRA is the authority for the centralization of all KYC records and details in the securities market. The client who wishes to open an account with a broker shall submit the KYC details. They can be submitted through the KYC Registration form with supporting documents. The Intermediary is responsible for conducting the initial KYC. The RI should also upload the details to the KRA system. The KYC details are accessible to all SEBI RIs for the same client. So once the client has undergone KYC with an RI, it is not necessary to repeat the same process again with other RIs.

It is compulsory for each client to be registered with any one of the various KRA registered intermediaries. This should be done before availing the benefits of any intermediary. Such benefits include Stock Broker, Mutual Fund Companies, Depository Participant, Portfolio Management Services (PMS) etc.

In-Person Verification (IPV) is part of the process of doing KRA-KYC registration of clients. KRA compliant clients are not required to undergo this process.

Importance Of IPV

The Prevention of Money Laundering Act, 2002 (PMLA), came into effect from 1 July 2005. The Act enforces that no one could use investment tools to hide their illegal wealth. Soon after, SEBI mandated that all intermediaries should adopt the KYC policy. It was also necessary to plan and install certain policies. The policies should follow vis-a-vis the guidelines on anti-money laundering measures.

Since 1 January 2011, KYC compliance has been made mandatory for all investors. This is irrespective of the amount invested and includes the following transactions:

a. New / Additional Purchases

b. Switching Transactions

c. First-time Registrations for SIP/ STP/ Flex STP/ FlexIndex/ DTP

d. Any SIP/STP/trigger-related products which were introduced after the enactment of the act

e-KYC (Know Your Customer) is a value-added feature that is offered by many financial institutions. E-kyc is useful for making the application process convenient. Investors can access it and upload the necessary documents. It can be done from the comfort of their home or office. As previously discussed, this is applicable to only SEBI-approved KRAs. For ex: CVL and CAMS can complete the e-KYC process. This means that digital KYC verification can be used for IPV as well.

New Norms For Digital KYC — Latest SEBI Guidelines

In a recent move on April 24, 2020, the SEBI has issued the latest guidelines pertaining to the digitisation of the KYC process. Some of the highlights are mentioned below:

1. Know Your Customer (KYC) and Customer Due Diligence (CDD) policies as part of KYC are the foundations of an effective Anti-Money Laundering process. The KYC process requires every SEBI registered intermediary (also known as ‘RI’) to collect and verify the Proof of Identity (PoI) and Proof of Address (PoA) from the investor.

2. The provisions as laid down under the Prevention of Money-Laundering Act, 2002, Prevention of Money-Laundering (Maintenance of Records) Rules, 2005, SEBI Master Circular on Anti Money Laundering (AML) dated October 15, 2019 and relevant KYC / AML circulars issued from time to time shall continue to remain applicable. Further, the SEBI registered intermediary shall continue to ensure to obtain the express consent of the investor before undertaking online KYC.

3. SEBI, from time to time has issued various circulars to simplify the process of KYC by investors / RIs. Constant technology evolution has led to multiple innovative platforms being created. These allow investors to complete the KYC process online. SEBI held discussions with various market participants and based on their feedback, technology like Aadhar-based e-Sign service which can facilitate online KYC will now be used. This is done with a view to allow ease of doing business in the securities market.

4. New regulations allow Investor’s KYC to be completed through an online / App-based KYC. There is also provision for in-person verification through video, online submission of Officially Valid Document (OVD) / other documents under eSign. It allows the introduction of VideoKYC, which was also allowed by RBI for the banking sector earlier this year. (Click here to read more about RBI Guidelines for VideoKYC)

5. SEBI registered intermediary may implement their own Application (App) for undertaking online KYC of investors. The App shall facilitate taking photographs, scanning, acceptance of OVD through Digilocker, video capturing in a live environment, usage of the App only by authorized persons of the RI.

6. The guidelines also allow RIs to undertake the VIPV(Video In-Person Verification) of an individual investor through their App. This is done to ease investor onboarding.

How Digital KYC Can Help Financial Institutions In The Securities Market

The latest SEBI guidelines have allowed ease of convenience to digitize the KYC process. This will be beneficial for financial institutions in the securities market. Previously banks, telecom, and other financial services providers used to deal with photocopies. The customer’s original ID proof was physically examined for conducting KYC verification. The conventional process of opening a DEMAT account can often become quite complex. It is also time-consuming and requires significant manpower.

The advantages to financial institutions in using eKYC are as follows:

- Paperless verification

- Cost-effective

- Prevents fraud

- Real-time identity verification

- Transparent

- Consent based to protect user privacy

E-KYC and VideoKYC — The New Age Digital KYC

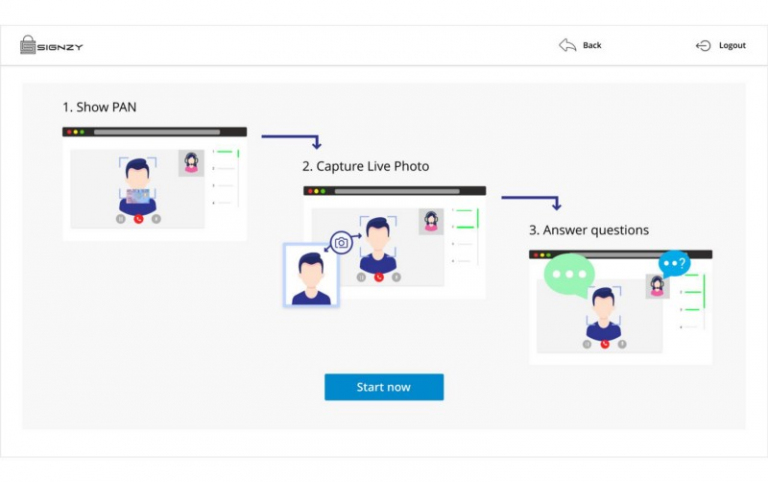

At Signzy, we offer a unique e-KYC solution known as RealKYC. The solution offers KYC collection as well as background verification and checks.

Advantages of RealKYC

- Secure System: A customer’s trading/DEMAT account information is secure. This is because the entire process is online. Identity theft, fraud, loan scams, money laundering, the flow of black money, etc. are all minimized with RealKYC.

- Efficient Communication: The data can be effectively relayed in a precise and timely fashion. There is no need for constant back and forth. Most details are published automatically unlike manual KYC.

- ‘Free of Cost’ Process: RealKYC verification doesn’t charge any extra amount to the customer. A company or institution may need to pay automation costs of installing verification systems for the long-run.

- Faster processing: The RealKYC service is completely automated online. This implies that KYC information can be transferred in real-time and does not require any manual intervention. The paper-based KYC process can be delayed for days and go up to weeks to get verified. Using the eKYC process reduces this to just a few minutes to verify and issue.

At Signzy, we have also introduced a new form of KYC verification called VideoKYC. This is a faster and more efficient form of KYC collection and verification. It conducts liveliness checks against the user. It also verifies the identification document against forgeries.

Advantages of using VideoKYC during investor onboarding

Signzy’s unique VideoKYC solution is compliant with RBI and SEBI guidelines. It has been the winner of several awards and accolades earlier this year. Here are some highlights of the product advantages:

- Higher Application Accuracy

- Plug and Play solution, swift Go-To-Market

- Comprehensive Training Program

- Competitive Advantage through customer delight

- 100% compliant with the latest RBI Mandate

- Exponentially increase Scale of Operations

- Reduced back office overheads (upto 70%)

- Reduction in customer Drop-offs (upto 50%)

- Platform Agnostic, support multiple communication channels

Conclusion

Over the last two decades, the securities market in India has witnessed structural reforms. This abolishes the century-old practices of trading and settlement. This has been possible due to the advent of technology that has created a nationwide network. It has enabled the market participants to interface from any corner in the country. With the new regulations and compliance norms, Digital KYC will soon become the standard for KYC collection in the market.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Visit www.signzy.com for more information about us.

You can reach out to our team at reachout@signzy.com

Written By:

Signzy

Written by an insightful Signzian intent on learning and sharing knowledge.