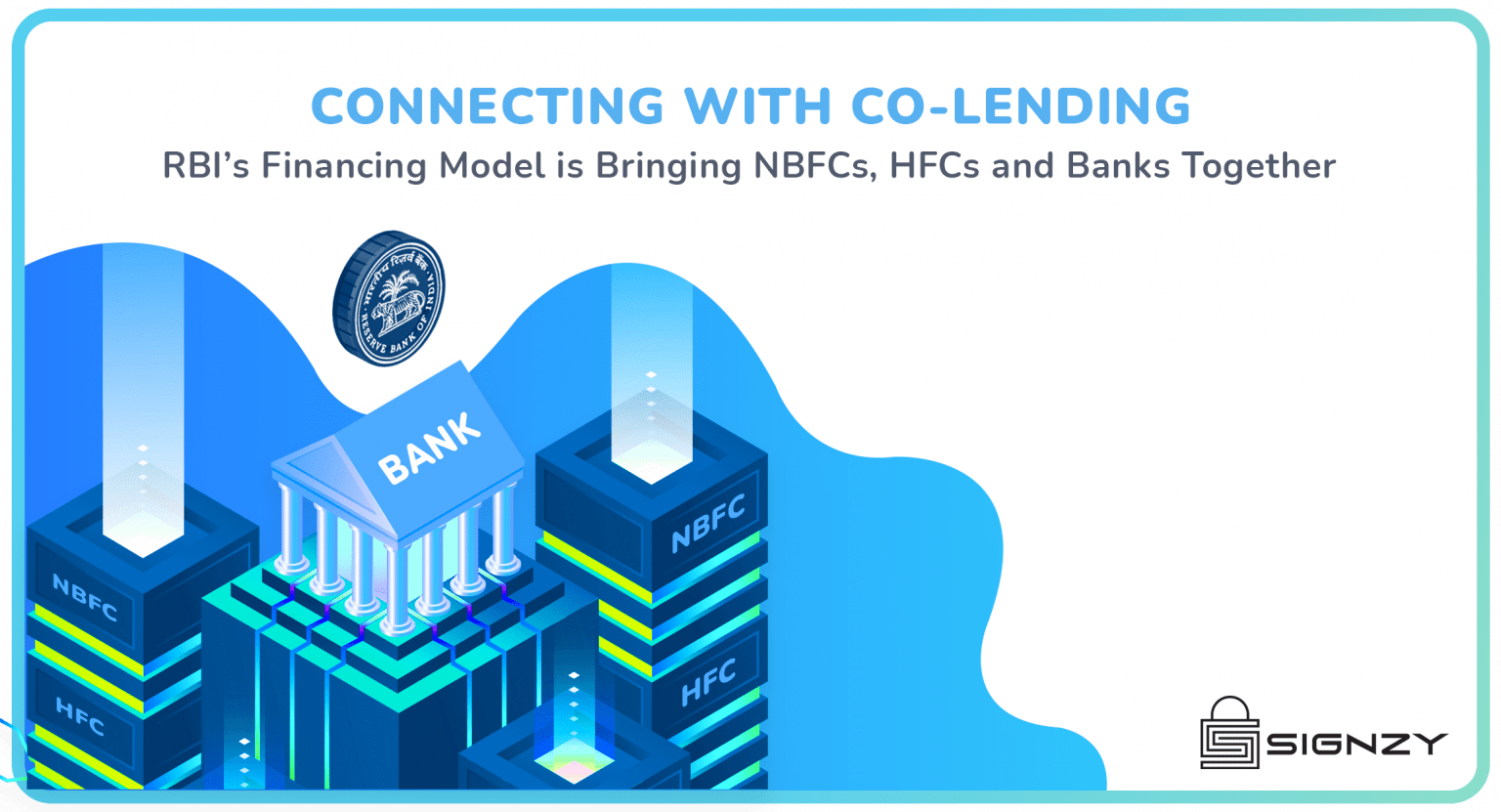

Connecting With Co-Lending- RBI’s Financing Model Is Bringing NBFCs, HFCs And Banks Together

October 22, 2021

4 minutes read

India’s aspirations for developing an entrepreneur-friendly economy largely depend on provisions of financial assistance for promising ventures. The major hurdle a new vendor seeking to establish his business finds in the country is mostly in the form of financial challenges. Even for the working community, financial aids and loans are very necessary solutions. That’s why 77% of working individuals in India rely on personal loans to merely make ends meet.

Most of these loans are for medical emergencies, MSME expenses, or family needs that may include education, weddings, and home renovations. The majority of the rural population does not have proper access to avail loans at banks. Hence, they seek private firms and local lenders.

As a resolution to the problem, RBI approves co-lending initiatives. Banks and Non-Banking Financial Companies(NBFCs) are exploring such venues, to generate a synergistic opportunity. This model of lending can certainly help India’s priority sectors in a great aspect.

Although co-lending processes have been around for some time in the BFSI sector, in November 2020, the Reserve bank of India furnished guidelines to ease non-bank lenders’ liquidity crisis. It enhances credit flow to dynamic and, productive sectors. Banks and NBFCs are increasingly exploring opportunities for co-lending

What Is The Co-Lending Model(CLM)?

The co-lending model includes the involvement of a bank and an NBFC. Both the lender firms partner to disburse loans to their customers. The RBI’s CLM model approves all registered NBFCs, including HFCs(Housing Finance Companies) to co-lend loans by partnering with banks.

The process involves Banks leveraging balance sheet strength which houses the majority of the whole loan amount while the NBFCs and HFCs enable origination and smooth collection. In essence, banks can lend to registered NBFCs and HFCs. These Institutions pass it on to individuals and organizations in priority sectors. This is because NBFCs and HFCs have greater reach than banks in many parts of the country.

The customers enter into a loan agreement with NBFCs while the latter acts as a single-point interface for the same borrowers. This agreement contains all the features of the prescribed arrangement including the roles and responsibilities of banks and NBFCs. The lenders decide upon an all-inclusive, reasonable interest rate for the ultimate borrower.

The target of this initiative is to better the credit flow of the priority sectors, particularly the underserved and even the unserved sections. This is possible with the coupling of banks providing a lower cost of funds for the customer while the NBFC utilizes their greater reach.

In the statement issued in November 2020, RBI has also emphasized that it strongly prescribes a part of the bank lending must help developmental activities. These include numerous divisions under the priority sector such as agriculture, housing, MSMEs, etc. The norms determine net bank credit(NBC) for each type of bank. Private and public banks lend 40% of NBC while foreign banks lend 32% of their NBC.

The Benefits Of Co-Lending

CLM initiative helps banks lend more funds to regions and sectors where they do not have sufficient reach. The more established reach from NBFCs helps banks meet the total PSL(Priority Sector Lending). The NBFCs on the other hand receive better and top-rated borrowers in their clientele.

It allows banks to expand and increase their lending business while giving NBFCs to source clients, disburse a part of the loan and perform credit appraisals. The end borrower gains accessibility to loans and borrowing options at affordable and competitive rates. In effect, a mass of the population receives inclusion in the booming financial ecosystem.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Visit www.signzy.com for more information about us.

You can reach out to our team at reachout@signzy.com

Written By:

Signzy

Written by an insightful Signzian intent on learning and sharing knowledge.