- Associations with high-risk countries can result in fines or investigations, even if unintentional, due to perceived non-compliance with anti-money laundering laws.

- Operating in or transacting with high-risk countries can block access to international markets due to AML-driven trade restrictions.

- Half of all money laundering cases stem from weak defences in financial institutions, creating a systemic blind spot for crime to thrive.

Now, it’s not about knowing which countries are high-risk anymore.

It’s about the hidden price of not knowing.

Because that next routine transaction could be the one that puts your entire business under the microscope.

Let’s understand it like this:

Think of the global financial system as a massive highway network.

Most lanes have speed cameras, traffic rules, and police patrols.

But some routes have fewer checkpoints and dimmer street lights. Not because they’re broken, but because they’re built differently. These routes attract more traffic – and not always the kind you’d want on your roads.

Below, we map out exactly which countries pose the highest AML risks in 2024 – and how to handle transactions with them.

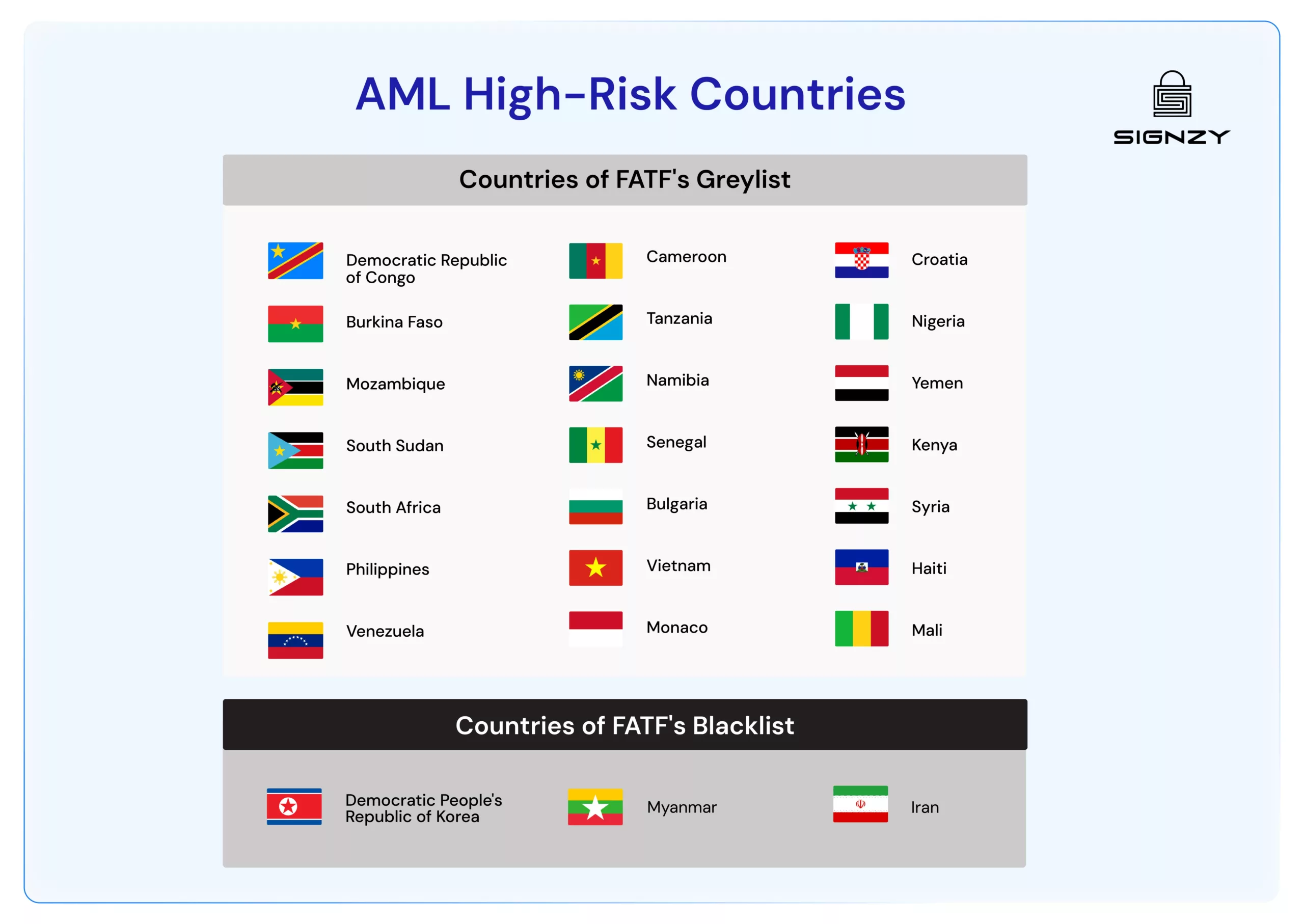

List of AML High-Risk Countries

The Financial Action Task Force (FATF), the global watchdog setting international standards for fighting financial crime has currently flagged 24 countries as “high-risk” jurisdictions.

Countries are classified after evaluation across multiple technical criteria, providing a measured assessment of money laundering and terrorism financing risks.

There are 2 main classes of AML high-risk countries.

- FATF Blacklist: High-Risk Jurisdictions Subject to a Call for Action (Consists 3 countries)

- FATF Greylist: Jurisdictions under Increased Monitoring (Consist 21 countries)

FATF blacklist (High-Risk Jurisdictions Subject to a Call for Action) is the highest risk category and demands comprehensive AML transaction monitoring and due diligence. As of October 2024, it consists of three countries:

- Democratic People’s Republic of Korea

- Myanmar

- Iran

For these jurisdictions, severe deficiencies in anti-money laundering and counter-terrorism financing frameworks demand immediate attention.

The implications reach far beyond simple monitoring – financial institutions must apply their most stringent controls and, in many cases, implement specific countermeasures to protect the global financial system.

Countries of FATF’s greylist (Jurisdictions under Increased Monitoring) are also considered as “high-risk”. However, unlike the blacklist, it represents countries actively working with FATF to resolve identified weaknesses.

As of October 2024, these 21 jurisdictions include:

- Democratic Republic of Congo

- Burkina Faso

- Mozambique

- South Sudan

- South Africa

- Philippines

- Venezuela

- Cameroon

- Tanzania

- Namibia

- Senegal

- Bulgaria

- Vietnam

- Monaco

- Croatia

- Nigeria

- Yemen

- Kenya

- Syria

- Haiti

- Mali

This list saw significant changes in October 2024, with Angola, Algeria, Côte d’Ivoire, and Lebanon being added, while Senegal demonstrated sufficient progress to exit the list.

Recent Changes in AML High-Risk Countries List

The FATF’s evaluation process is systematic and responsive, with updates occurring three times each year. This regular assessment cycle helps maintain the accuracy and relevance of risk classifications while providing countries with clear pathways toward improvement.

2024 has been marked by several notable changes:

- February: UAE, Barbados, Gibraltar, and Uganda demonstrated sufficient progress to exit monitoring, while Kenya and Namibia entered the process

- June: Jamaica and Türkiye completed their improvement programs, as Monaco and Venezuela began theirs

- October: Senegal’s exit coincided with four new jurisdictions entering monitoring

More About AML High-Risk Countries

In the context of Anti-Money Laundering (AML), when FATF designates a jurisdiction as “high-risk,” it signals specific concerns about that country’s ability to prevent and detect money laundering activities.

This designation stems from a thorough evaluation of how effectively countries implement AML controls and safeguards.

A high-risk jurisdiction typically displays significant weaknesses in:

- Investigation and enforcement mechanisms

- Legal frameworks and regulatory systems

- International cooperation effectiveness

- Preventive measure implementation

- Transaction monitoring capabilities

- Beneficial ownership transparency

- Cross-border movement controls

- Supervisory framework strength

- Quality of AML/CFT regulations

These weaknesses don’t exist in isolation. They represent gaps in the protective measures that help maintain the integrity of global finance.

It’s essential to recognize that ‘high-risk’ doesn’t mean ‘no business’ – rather, it signals the need for additional care and attention. It enables businessesto build appropriate safeguards while maintaining necessary business relationships.

In short – the “high-risk” designation serves a constructive purpose.

How to Work With High-Risk Jurisdictions

Operating in high-risk jurisdictions brings additional responsibilities, yet these measures protect both the global financial system and legitimate business activities.

If you are working with any of the High-Risk Jurisdictions, below are some core operational requirements you must follow:

| Area | Key Requirements | Purpose |

| Transaction Monitoring | – Normal business pattern analysis – Volume and frequency tracking – Market-specific benchmarking – Seasonal variation monitoring | To identify genuine anomalies while respecting legitimate business patterns |

| Documentation | – Transaction records – Source of funds verification – Relationship reviews – Assessment reports – Regulatory filings | To maintain clear, verifiable records of all business activities |

| Risk Assessment | – Country risk evaluation – Industry analysis – Transaction pattern review – Risk monitoring – Framework updates | To maintain appropriate risk controls while supporting business growth |

While we could have included the enhanced due diligence requirements within the above table, it’s something you, as a business, need to give extra attention. That’s why we have dedicated an entire section detailing what you should know.

Enhanced Due Diligence Requirements

Working with high-risk jurisdictions brings additional responsibilities, but these requirements serve to protect all parties involved.

Institutions must obtain substantially more documentation for high-risk jurisdiction relationships. This includes certified copies of incorporation documents, detailed business plans, and comprehensive ownership structures.

Beyond basic transaction records, regulations also require specific documentation of funds moving to or from high-risk jurisdictions:

- Clear documentation of expected transaction types and volumes

- Evidence of legitimate business activities in high-risk locations

- Full details of major business partners and their jurisdictions

- Banking references from regulated financial institutions

- Evidence of import/export licenses where applicable

- Detailed transaction records showing clear patterns

- Tax returns or audited financial statements

Suspicious Activity Reports (SARs) must be filed for transactions of $5,000 or more if suspicious activity is detected. Relationship reviews must occur at least every 180 days, with full documentation updates annually.

These requirements might seem extensive, but they protect both institutions and their clients while enabling legitimate business to continue. Clear documentation and consistent processes help manage these relationships effectively.

Conducting EDD with Technology

Enhanced Due Diligence requirements might seem daunting at first, but modern technology makes these extra steps more manageable.

Identity verification solutions can help streamline the verification of 10% ownership thresholds through automated document checks and biometric verification while maintaining the high standards needed for high-risk relationships.

For day-to-day requirements, transaction monitoring systems can automatically track patterns and flag unusual activities at the $5,000 threshold.

These tools, combined with automated UBO registries and continuous screening solutions, help maintain security while letting legitimate business flow smoothly.

Signzy’s unified platform brings all these capabilities together. Through a single interface, institutions can efficiently manage document validation, biometric verification, UBO checks, and continuous monitoring for high-risk relationships. This integrated approach helps maintain compliance while reducing the operational complexity of enhanced due diligence requirements.

FAQs

What makes a country "high-risk" for AML purposes?

A country is designated high-risk when FATF identifies significant weaknesses in its ability to prevent money laundering, including gaps in regulations, monitoring, and enforcement capabilities.

How often does FATF update its high-risk country lists?

FATF updates its lists three times annually – typically in February, June, and October – reflecting changes in countries’ AML frameworks and compliance levels.

What's the difference between FATF's blacklist and grey list?

The blacklist (Call for Action) requires countermeasures for severe deficiencies, while the grey list (Increased Monitoring) indicates countries actively working to address identified weaknesses.

Are business relationships with high-risk countries prohibited?

No, but they require enhanced due diligence, more frequent monitoring, and additional documentation to ensure transactions remain compliant and legitimate.